Ferhat Erata’s ML/AI Study Notes

Comprehensive notes covering machine learning fundamentals, optimization theory, math foundations, deep learning, sequence models, LLM training pipelines, and distributed systems.

Quick Navigation

| Topic | Key Areas |

|---|---|

| 1. Learning Through Examples | Linear/Logistic Regression, MLP, Backprop, CNNs |

| 2. Core Theory | Gradient Descent, Adam/AdamW, Learning Rates |

| 3. Math Foundations | Linear Algebra, Probability, Calculus |

| 4. ML Fundamentals | Bias-Variance, Overfitting, Evaluation |

| 5. Optimization | SGD, Momentum, Regularization |

| 6. Sequence Models | RNNs, LSTMs, Transformers |

| 7. LLM Training | Pretraining, SFT, RLHF, DPO |

| 8. Distributed Training | DDP, Tensor/Pipeline Parallelism, ZeRO |

| 9. Reinforcement Learning | MDPs, Q-Learning, Policy Gradients, PPO |

| 10. ML Systems | SPMD, Collectives, Memory Analysis |

| 11. Advanced Transformers | MoE, Flash Attention, KV-Cache, Mamba |

| 12. Question Bank | Q&A, ML Debugging, System Design |

Part 1: Learning Through Examples

1.1 What is Machine Learning?

Machine learning is about finding patterns in data. Instead of writing explicit rules, we:

- Define a model with adjustable parameters (weights)

- Define a loss function that measures how wrong we are

- Use an algorithm to adjust parameters to reduce the loss

The goal: Find parameter values that make our model’s predictions match the real data as closely as possible.

Data → [Model with parameters w] → Predictions

↓

Compare to real answers

↓

Loss (error)

↓

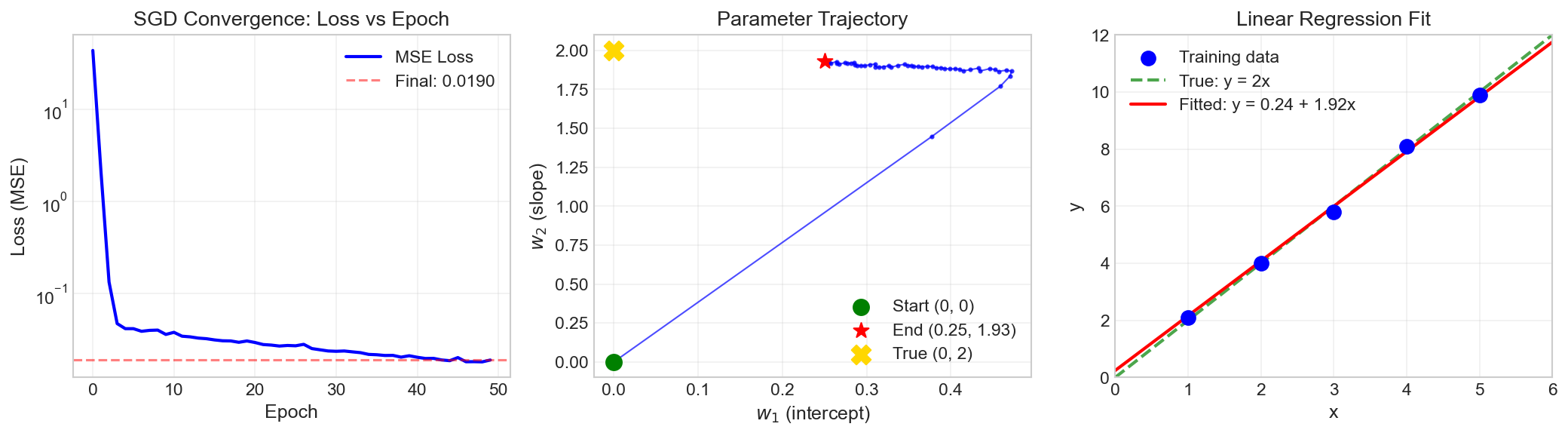

Adjust w to reduce loss ← Gradient descent!1.2 Simple Linear Regression

The Problem

You have data about houses: square footage (x) and sale price (y). You want to predict price from size.

| House | Size (sq ft) | Price ($1000s) |

|---|---|---|

| 1 | 1000 | 200 |

| 2 | 1500 | 280 |

| 3 | 2000 | 350 |

| 4 | 2500 | 400 |

| 5 | 3000 | 500 |

The Model: A Line

We assume price is (roughly) linear in size:

\[ \hat{y} = w \cdot x + b \]

where:

- \(x\) = input (square footage)

- \(\hat{y}\) = predicted price

- \(w\) = weight (slope of the line — how much price increases per sq ft)

- \(b\) = bias (intercept — base price)

Our job: Find the best values of \(w\) and \(b\).

Visualizing Different Choices

Price ($1000s)

↑

500 | * (3000, 500)

400 | * (2500, 400)

350 | * (2000, 350)

280 | * (1500, 280)

200 | * (1000, 200)

|________________________→ Size (sq ft)

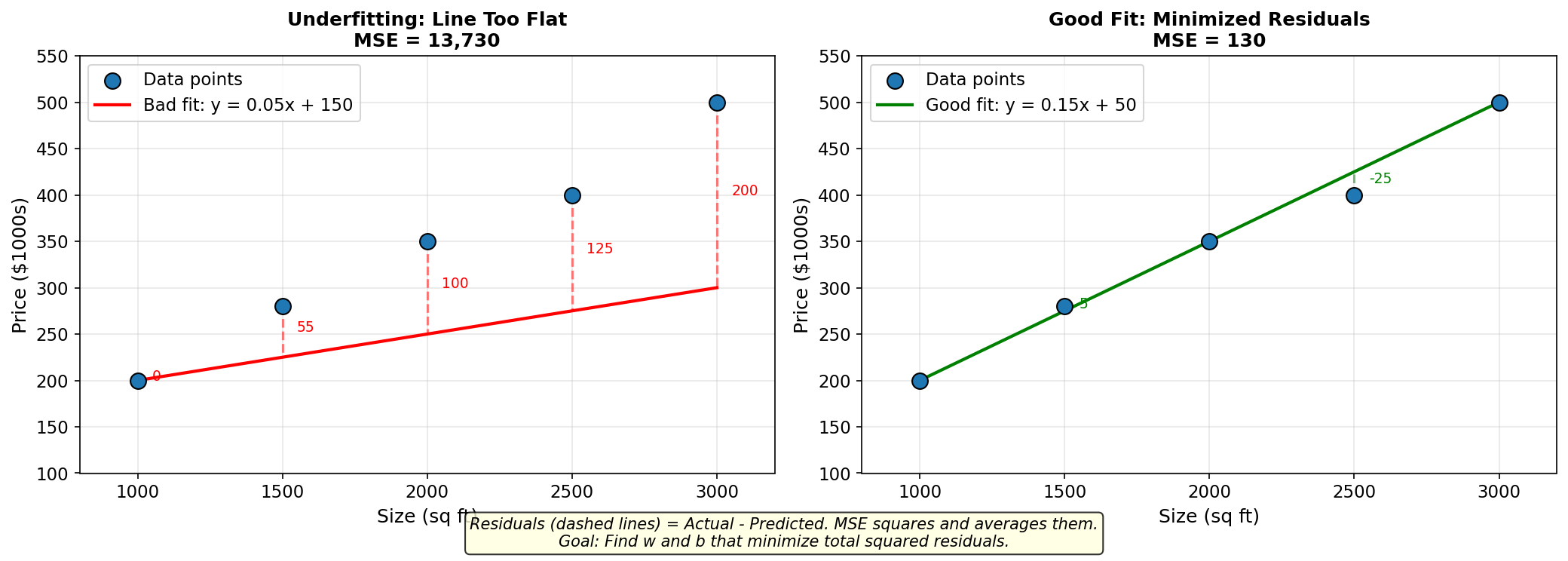

1000 1500 2000 2500 3000Bad line (\(w = 0.05\), \(b = 150\)):

\[\hat{y} = 0.05 \cdot x + 150\]

| x | Actual y | Predicted \(\hat{y}\) | Error |

|---|---|---|---|

| 1000 | 200 | 200 | 0 |

| 1500 | 280 | 225 | -55 |

| 2000 | 350 | 250 | -100 |

| 2500 | 400 | 275 | -125 |

| 3000 | 500 | 300 | -200 |

The line is too flat!

Better line (\(w = 0.15\), \(b = 50\)):

\[\hat{y} = 0.15 \cdot x + 50\]

| x | Actual y | Predicted \(\hat{y}\) | Error |

|---|---|---|---|

| 1000 | 200 | 200 | 0 |

| 1500 | 280 | 275 | -5 |

| 2000 | 350 | 350 | 0 |

| 2500 | 400 | 425 | +25 |

| 3000 | 500 | 500 | 0 |

Much better!

Figure: Comparing a bad

fit (left) with large residuals (MSE = 13,730) to a good fit

(right) with minimized residuals (MSE = 130). The dashed

lines show the errors — gradient descent minimizes the sum

of squared errors.

Figure: Comparing a bad

fit (left) with large residuals (MSE = 13,730) to a good fit

(right) with minimized residuals (MSE = 130). The dashed

lines show the errors — gradient descent minimizes the sum

of squared errors.

The Loss Function: Mean Squared Error

How do we quantify “how wrong” a line is? Use Mean Squared Error (MSE):

\[ \text{Loss} = \frac{1}{N} \sum_{i=1}^{N} (y_i - \hat{y}_i)^2 = \frac{1}{N} \sum_{i=1}^{N} (y_i - (w \cdot x_i + b))^2 \]

Why squared?

- Positive: Errors don’t cancel out

- Penalizes big errors more: An error of 100 contributes \(100^2 = 10000\), not just 100

- Smooth: Has nice derivatives for optimization

For our “bad line”: \[ \text{Loss} = \frac{1}{5}(0^2 + 55^2 + 100^2 + 125^2 + 200^2) = \frac{1}{5}(0 + 3025 + 10000 + 15625 + 40000) = 13730 \]

For our “better line”: \[ \text{Loss} = \frac{1}{5}(0^2 + 5^2 + 0^2 + 25^2 + 0^2) = \frac{1}{5}(0 + 25 + 0 + 625 + 0) = 130 \]

Lower loss = better fit!

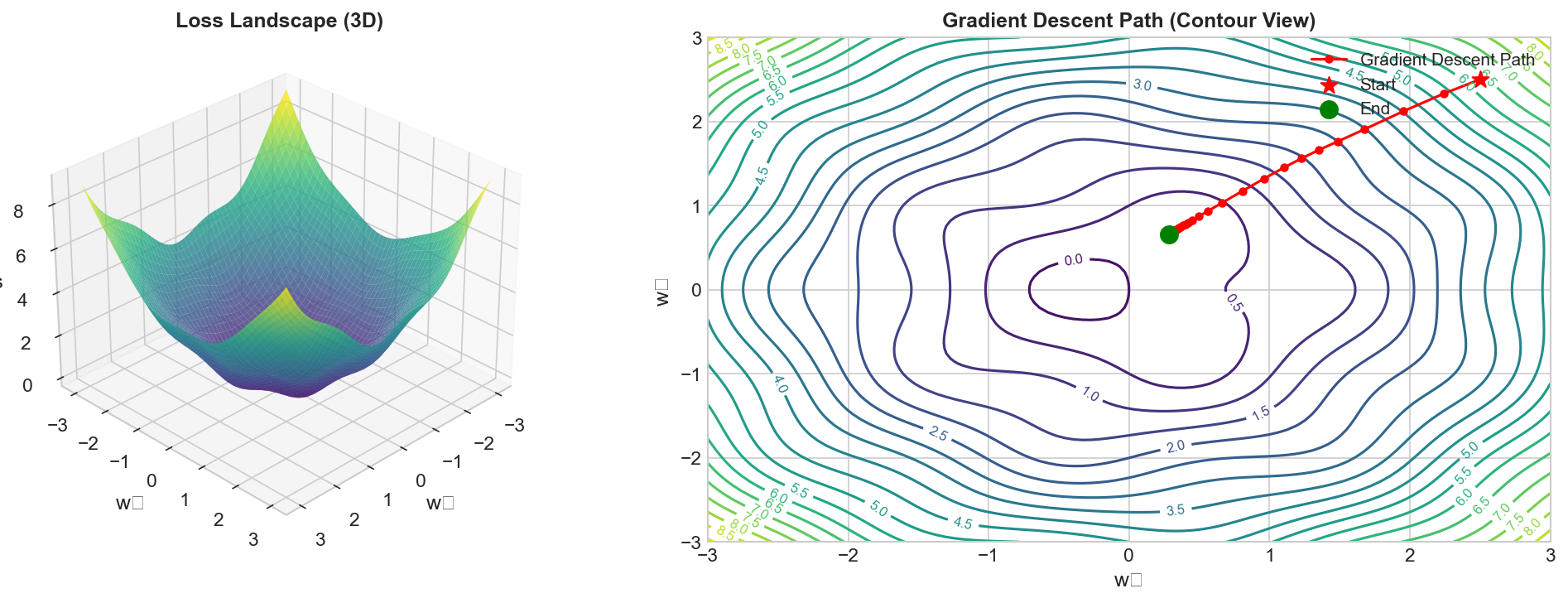

1.3 Gradient Descent: Finding the Best Line

The Optimization Problem

We want to find \((w^*, b^*)\) that minimize the loss:

\[ (w^*, b^*) = \arg\min_{w, b} \frac{1}{N} \sum_{i=1}^{N} (y_i - (w \cdot x_i + b))^2 \]

For simple linear regression, there’s a closed-form solution. But for neural networks, there isn’t — we need gradient descent.

Figure: 3D visualization of a

loss landscape showing the optimization surface and gradient

descent path.

Figure: 3D visualization of a

loss landscape showing the optimization surface and gradient

descent path.

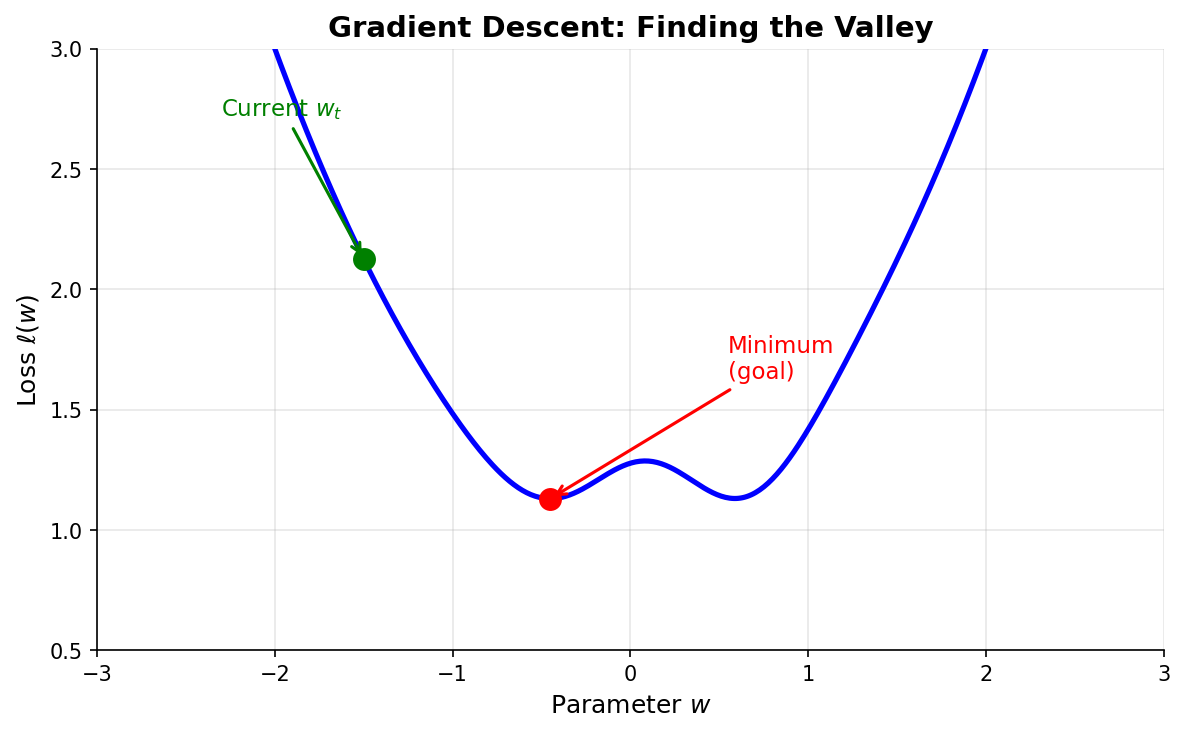

The Key Idea

The loss is a function of \(w\) and \(b\). If we plot loss vs parameters, we get a surface:

Figure: The

loss function forms a landscape over parameter space.

Gradient descent finds the minimum (valley) by taking steps

in the direction of steepest descent.

Figure: The

loss function forms a landscape over parameter space.

Gradient descent finds the minimum (valley) by taking steps

in the direction of steepest descent.

Gradient descent: Start somewhere, repeatedly take small steps “downhill” until you reach the bottom.

What is a Gradient? (Intuitive Explanation)

Before diving into the math, let’s build intuition about what a gradient actually is.

The core idea: A gradient is a vector that points in the direction of steepest increase of a function.

Physical analogy: Imagine standing on a hilly terrain. The gradient at your location is like an arrow pointing directly uphill—the direction you’d go if you wanted to climb as steeply as possible. If you want to descend to the valley (minimize elevation), you walk in the opposite direction of this arrow.

Why is it a vector? Because we have multiple parameters to adjust! If we have two parameters (\(w\) and \(b\)), the gradient has two components:

- The first component tells us: “How much does the loss change if I nudge \(w\) a tiny bit?”

- The second component tells us: “How much does the loss change if I nudge \(b\) a tiny bit?”

Together, these form a vector that points toward the steepest uphill direction in the 2D parameter space.

Mathematical definition: The gradient of a function \(f(w, b)\) is the vector of all its partial derivatives:

\[\nabla f = \begin{bmatrix} \frac{\partial f}{\partial w} \\ \frac{\partial f}{\partial b} \end{bmatrix}\]

Each partial derivative measures the “sensitivity” of the output to changes in one input while holding others fixed.

Key insight for optimization: Since the gradient points uphill, we go the opposite direction to minimize the loss: \[\text{new parameters} = \text{old parameters} - \alpha \cdot \nabla \text{Loss}\]

where \(\alpha\) is the learning rate (step size).

The Gradient: Which Way is Downhill?

The gradient tells us the direction of steepest uphill. So we go the opposite direction!

For our linear regression:

\[ \frac{\partial \text{Loss}}{\partial w} = \frac{1}{N} \sum_{i=1}^{N} -2x_i(y_i - (w \cdot x_i + b)) = -\frac{2}{N} \sum_{i=1}^{N} x_i(y_i - \hat{y}_i) \]

\[ \frac{\partial \text{Loss}}{\partial b} = \frac{1}{N} \sum_{i=1}^{N} -2(y_i - (w \cdot x_i + b)) = -\frac{2}{N} \sum_{i=1}^{N} (y_i - \hat{y}_i) \]

Intuition:

- If predictions are too low (\(y_i - \hat{y}_i > 0\)), we need to increase \(w\) and \(b\)

- The gradient is negative → subtracting it makes \(w\) and \(b\) bigger ✓

The Update Rule

\[ w_{\text{new}} = w_{\text{old}} - \alpha \cdot \frac{\partial \text{Loss}}{\partial w} \]

\[ b_{\text{new}} = b_{\text{old}} - \alpha \cdot \frac{\partial \text{Loss}}{\partial b} \]

where \(\alpha\) is the learning rate (step size).

Concrete Example: Step by Step

Let’s use our housing data: \(x = [1000, 1500, 2000, 2500, 3000]\), \(y = [200, 280, 350, 400, 500]\)

Initialize: \(w = 0.0\), \(b = 0.0\), \(\alpha = 0.0000001\) (tiny because our \(x\) values are large)

Step 1: Compute predictions \[ \hat{y} = [0, 0, 0, 0, 0] \]

Step 2: Compute errors \[ y - \hat{y} = [200, 280, 350, 400, 500] \]

Step 3: Compute gradients \[ \frac{\partial L}{\partial w} = -\frac{2}{5}(1000 \cdot 200 + 1500 \cdot 280 + 2000 \cdot 350 + 2500 \cdot 400 + 3000 \cdot 500) \]

\[ = -\frac{2}{5}(200000 + 420000 + 700000 + 1000000 + 1500000) = -\frac{2}{5}(3820000) = -1528000 \]

\[ \frac{\partial L}{\partial b} = -\frac{2}{5}(200 + 280 + 350 + 400 + 500) = -\frac{2}{5}(1730) = -692 \]

Step 4: Update parameters \[ w = 0 - 0.0000001 \cdot (-1528000) = 0.1528 \]

\[ b = 0 - 0.0000001 \cdot (-692) = 0.0000692 \]

After just one step, \(w \approx 0.15\) — already close to the good value!

Repeat until loss stops decreasing.

Python Implementation

import numpy as np

# Data

X = np.array([1000, 1500, 2000, 2500, 3000])

y = np.array([200, 280, 350, 400, 500])

# Initialize parameters

w = 0.0

b = 0.0

learning_rate = 0.0000001

n = len(X)

# Gradient descent

for step in range(1000):

# Predictions

y_pred = w * X + b

# Loss (MSE)

loss = np.mean((y - y_pred) ** 2)

# Gradients

dw = -2/n * np.sum(X * (y - y_pred))

db = -2/n * np.sum(y - y_pred)

# Update

w = w - learning_rate * dw

b = b - learning_rate * db

if step % 100 == 0:

print(f"Step {step}: w={w:.4f}, b={b:.4f}, loss={loss:.2f}")

# Final: Step 900: w=0.1480, b=53.7000, loss=133.831.4 Logistic Regression: Classification

The Problem: Binary Classification

Now instead of predicting a continuous value, we want to classify: Is this email spam or not?

| Contains “FREE” | Contains “!” | Has link | Label | |

|---|---|---|---|---|

| 1 | 1 | 1 | 1 | Spam (1) |

| 2 | 0 | 0 | 0 | Not spam (0) |

| 3 | 1 | 1 | 0 | Spam (1) |

| 4 | 0 | 1 | 1 | Not spam (0) |

| 5 | 1 | 0 | 1 | Spam (1) |

Why Linear Regression Fails

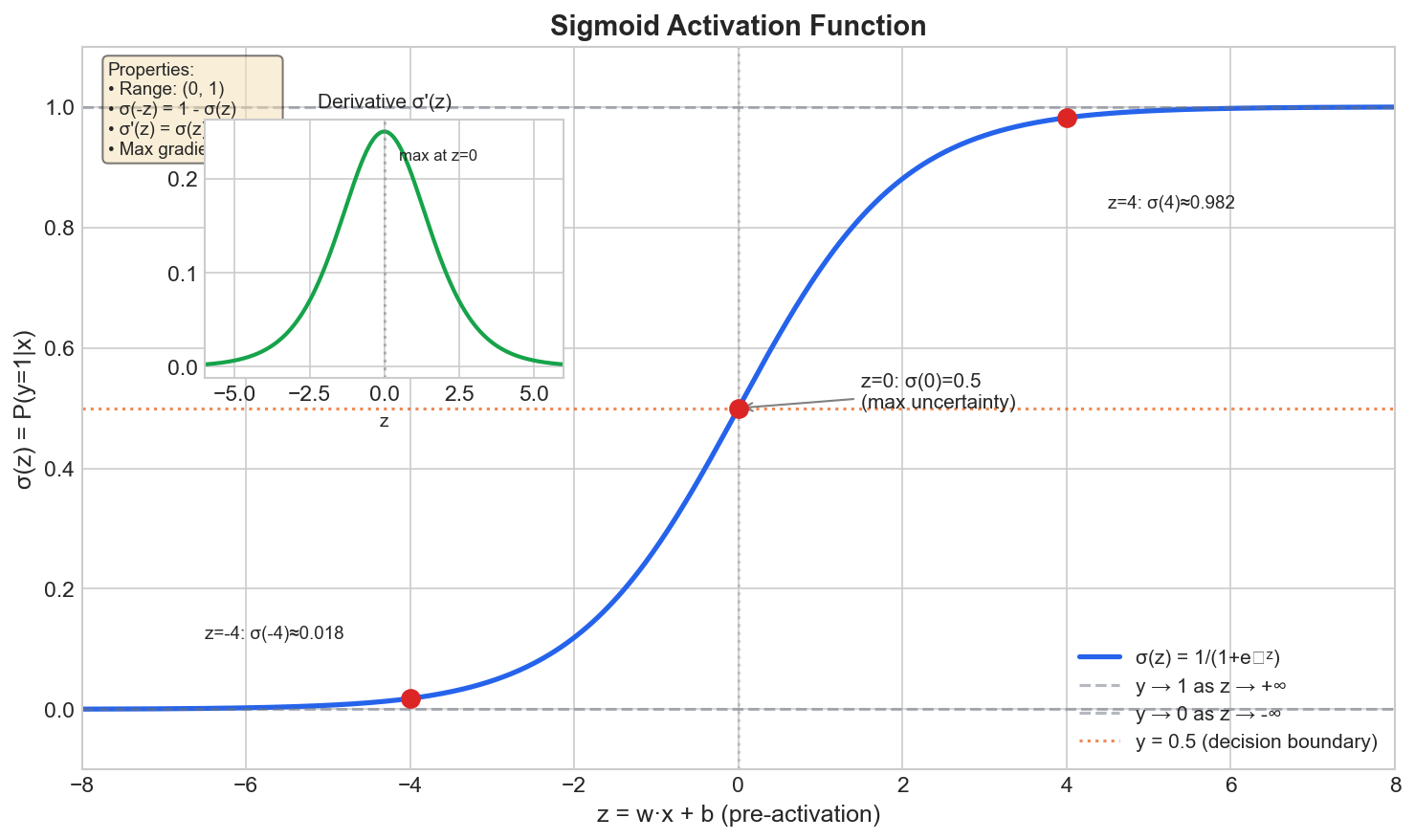

If we use \(\hat{y} = w_1 x_1 + w_2 x_2 + w_3 x_3 + b\), we might get outputs like \(-0.5\) or \(2.3\) — but we need probabilities between 0 and 1!

The Sigmoid Function

We “squash” the linear output through the sigmoid function:

\[ \sigma(z) = \frac{1}{1 + e^{-z}} \]

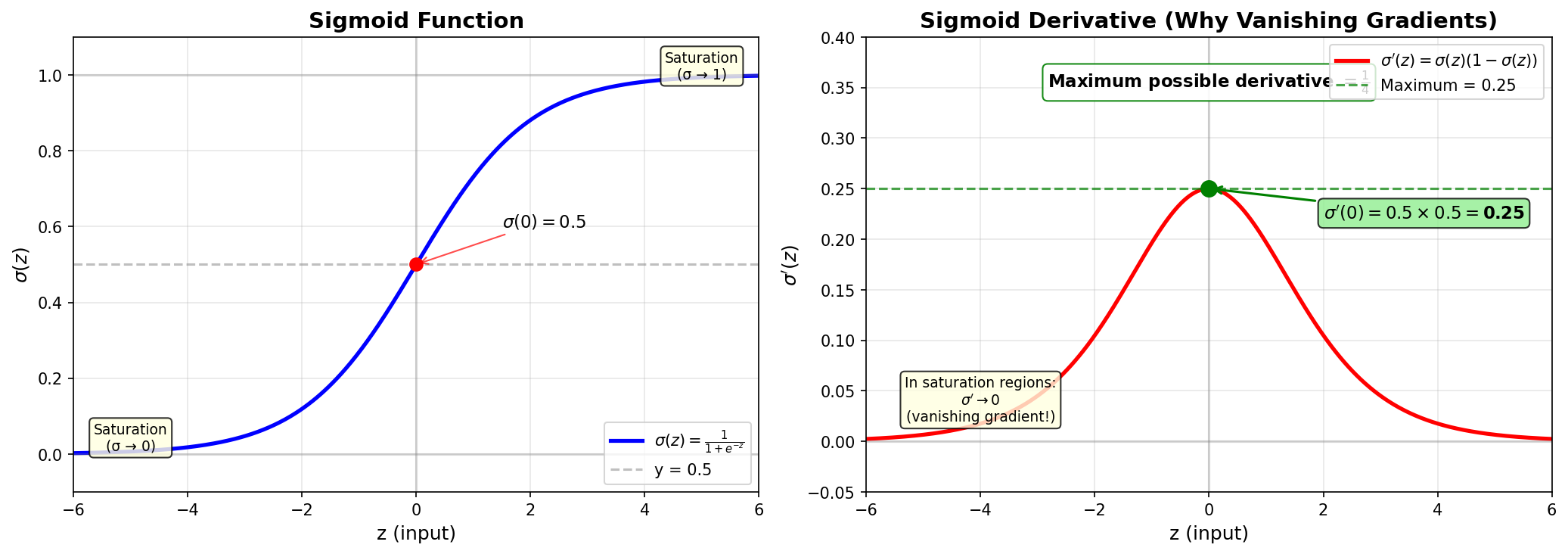

Figure: The sigmoid function

σ(z) = 1/(1+e^(-z)) squashes any input to a value between 0

and 1.

Figure: The sigmoid function

σ(z) = 1/(1+e^(-z)) squashes any input to a value between 0

and 1.

Properties:

- Always outputs between 0 and 1 ✓

- \(\sigma(0) = 0.5\)

- \(\sigma(\text{large positive}) \approx 1\)

- \(\sigma(\text{large negative}) \approx 0\)

Deriving the Sigmoid Derivative (Chain Rule Example)

Understanding the sigmoid derivative is crucial for backpropagation. Let’s derive it step-by-step using the chain rule.

Starting point: \[\sigma(z) = \frac{1}{1 + e^{-z}} = (1 + e^{-z})^{-1}\]

Step 1: Apply the chain rule

Let \(u = 1 + e^{-z}\), so \(\sigma = u^{-1}\)

We need \(\frac{d\sigma}{dz} = \frac{d\sigma}{du} \cdot \frac{du}{dz}\)

Step 2: Compute each part

Power rule: \(\frac{d\sigma}{du} = \frac{d}{du}(u^{-1}) = -u^{-2} = -\frac{1}{(1+e^{-z})^2}\)

Chain rule on exponential: \(\frac{du}{dz} = \frac{d}{dz}(1 + e^{-z}) = -e^{-z}\)

Step 3: Multiply

\[\frac{d\sigma}{dz} = -\frac{1}{(1+e^{-z})^2} \cdot (-e^{-z}) = \frac{e^{-z}}{(1+e^{-z})^2}\]

Step 4: Simplify to the elegant form

Notice that: \[\frac{e^{-z}}{(1+e^{-z})^2} = \frac{1}{1+e^{-z}} \cdot \frac{e^{-z}}{1+e^{-z}} = \sigma(z) \cdot \frac{e^{-z}}{1+e^{-z}}\]

And \(\frac{e^{-z}}{1+e^{-z}} = \frac{1+e^{-z}-1}{1+e^{-z}} = 1 - \frac{1}{1+e^{-z}} = 1 - \sigma(z)\)

Final result: \[\boxed{\sigma'(z) = \sigma(z)(1 - \sigma(z))}\]

This is remarkably elegant — the derivative depends only on the output, not the input!

Why the Maximum Derivative is 1/4 (and Why It Matters)

The sigmoid derivative \(\sigma'(z) = \sigma(z)(1 - \sigma(z))\) has a maximum value of 0.25. Let’s prove this and understand its implications.

Figure: The sigmoid function

and its derivative. The derivative reaches its maximum of

0.25 at z=0, where σ(z)=0.5.

Figure: The sigmoid function

and its derivative. The derivative reaches its maximum of

0.25 at z=0, where σ(z)=0.5.

Step 1: Reframe the problem

Let \(y = \sigma(z)\). Since sigmoid outputs are in \((0, 1)\), we need to find the maximum of: \[f(y) = y(1 - y) = y - y^2 \quad \text{for } y \in (0, 1)\]

Step 2: Find the maximum

This is a downward-opening parabola. Taking the derivative: \[\frac{df}{dy} = 1 - 2y\]

Setting to zero: \(1 - 2y = 0 \Rightarrow y = 0.5\)

Step 3: Calculate the maximum value

\[f(0.5) = 0.5 \times (1 - 0.5) = 0.5 \times 0.5 = \boxed{0.25 = \frac{1}{4}}\]

What this means: At the optimal point (\(z = 0\), where \(\sigma(z) = 0.5\)), the gradient through a sigmoid is only 0.25. In the saturation regions (where \(\sigma \to 0\) or \(\sigma \to 1\)), the derivative approaches 0.

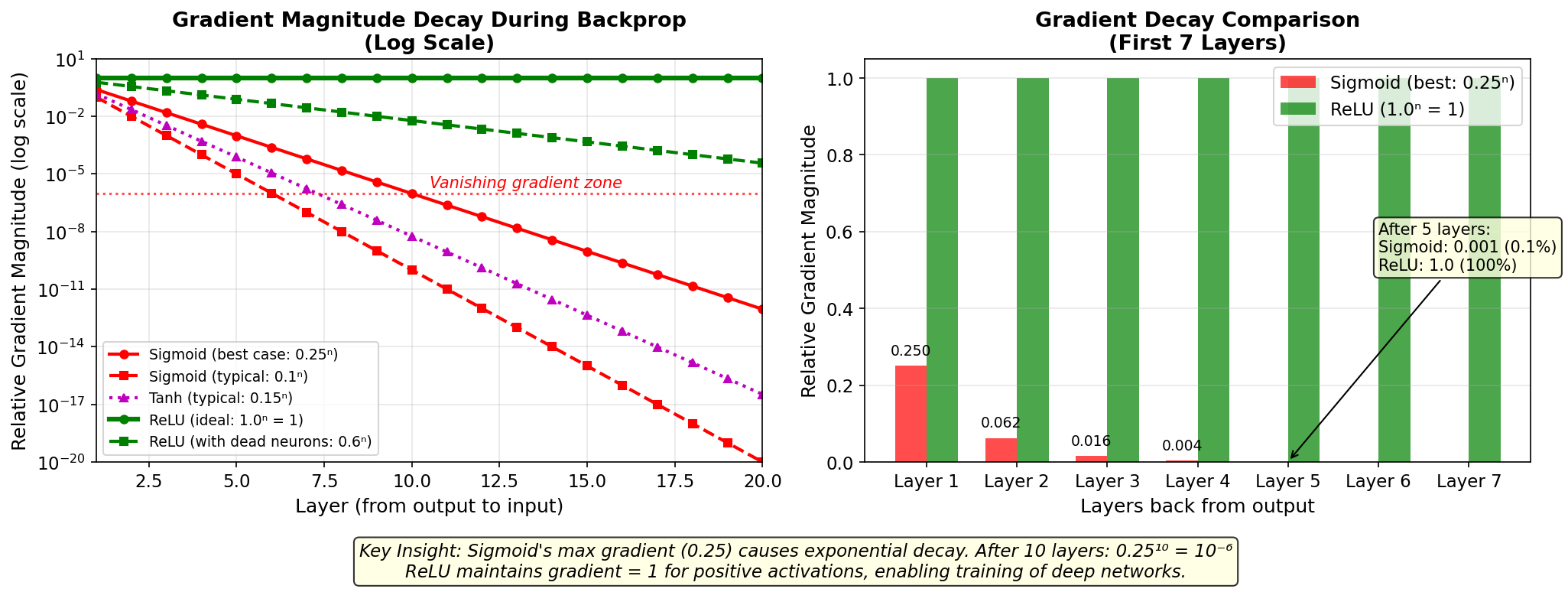

The Vanishing Gradient Problem

This maximum of 1/4 has catastrophic implications for deep networks:

During backpropagation, gradients are multiplied at each layer: \[\frac{\partial L}{\partial W_1} = \frac{\partial L}{\partial z_n} \cdot \sigma'(z_{n-1}) \cdot \sigma'(z_{n-2}) \cdots \sigma'(z_1)\]

Even in the best case (all neurons at \(\sigma = 0.5\)):

| Layers | Gradient Factor | Result |

|---|---|---|

| 5 | \(0.25^5\) | 0.001 (1/1000) |

| 10 | \(0.25^{10}\) | \(10^{-6}\) (one millionth!) |

| 20 | \(0.25^{20}\) | \(10^{-12}\) |

In practice, it’s worse: Neurons rarely sit at \(\sigma = 0.5\). In saturation regions, \(\sigma' \approx 0\), making gradients vanish even faster.

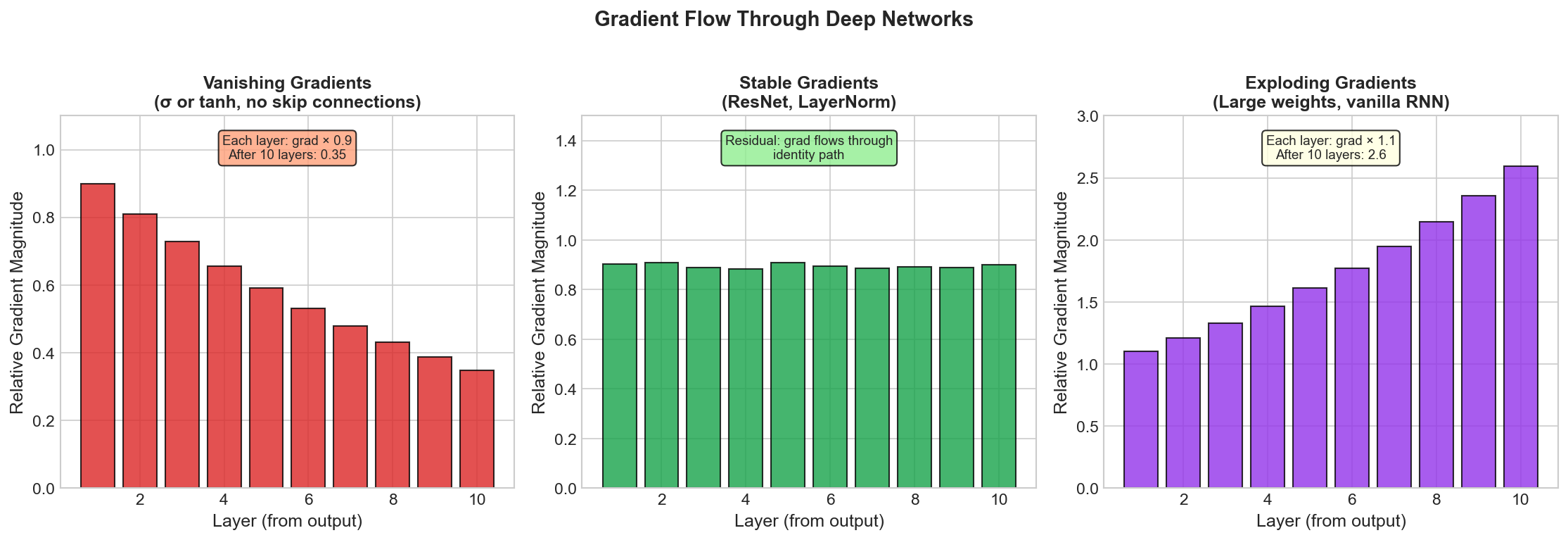

Symptoms of vanishing gradients: - Early layers (near input) barely update - Loss decreases very slowly - Deep networks fail to train

Figure:

Gradient magnitude decay during backpropagation for

different activation functions. Sigmoid’s max derivative of

0.25 causes exponential decay — after 10 layers, gradients

shrink to 10⁻⁶ (best case). ReLU maintains gradient = 1 for

positive activations, enabling training of very deep

networks. The bar chart shows how quickly sigmoid gradients

become negligible.

Figure:

Gradient magnitude decay during backpropagation for

different activation functions. Sigmoid’s max derivative of

0.25 causes exponential decay — after 10 layers, gradients

shrink to 10⁻⁶ (best case). ReLU maintains gradient = 1 for

positive activations, enabling training of very deep

networks. The bar chart shows how quickly sigmoid gradients

become negligible.

Figure: Comparison

of sigmoid and ReLU derivatives. ReLU has gradient = 1 for

positive inputs, avoiding exponential decay.

Figure: Comparison

of sigmoid and ReLU derivatives. ReLU has gradient = 1 for

positive inputs, avoiding exponential decay.

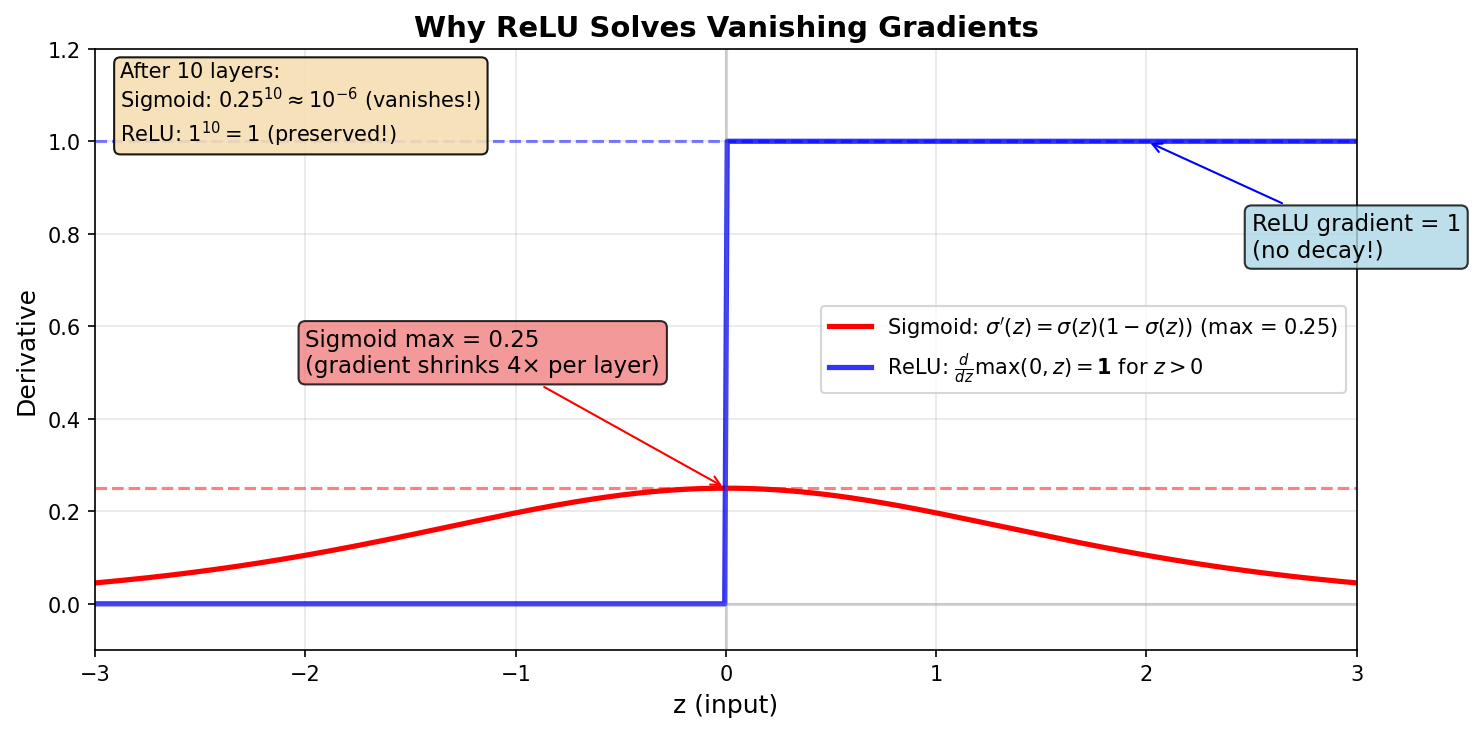

ReLU: The Solution to Vanishing Gradients

ReLU (Rectified Linear Unit) solves this problem:

\[\text{ReLU}(z) = \max(0, z)\]

ReLU derivative: \[\text{ReLU}'(z) = \begin{cases} 1 & \text{if } z > 0 \\ 0 & \text{if } z \leq 0 \end{cases}\]

Why ReLU works:

| Property | Sigmoid | ReLU |

|---|---|---|

| Max derivative | 0.25 | 1 |

| After 10 layers (best case) | \(0.25^{10} \approx 10^{-6}\) | \(1^{10} = 1\) |

| Gradient decay | Exponential | None! |

| Saturation | Both directions | Only negative |

The key insight: With ReLU, gradients pass through unchanged (multiplied by 1) for positive activations. There’s no exponential decay, so deep networks can actually train!

Trade-off: ReLU has “dead neurons” — if a neuron’s input is always negative, its gradient is always 0 and it never updates. Solutions include: - Leaky ReLU: Small gradient for negative inputs (\(0.01x\) instead of \(0\)) - ELU/GELU: Smooth alternatives with better properties

Interview Q: “Why do we use ReLU instead of sigmoid in hidden layers?”

A: Sigmoid has a maximum derivative of 0.25, causing vanishing gradients in deep networks. After just 10 layers, even in the best case, gradients shrink to \(0.25^{10} \approx 10^{-6}\). Early layers barely learn. ReLU has derivative = 1 for positive inputs, so gradients pass through without decay. This enables training of deep networks. The trade-off is “dead neurons” (gradient = 0 for negative inputs), addressed by variants like Leaky ReLU.

Logistic Regression Model

\[ P(y=1|x) = \sigma(w^\top x + b) = \frac{1}{1 + e^{-(w^\top x + b)}} \]

Interpretation: “The probability this email is spam, given its features.”

The Loss Function: Binary Cross-Entropy

For classification, we use cross-entropy loss (not MSE):

\[ \text{Loss} = -\frac{1}{N}\sum_{i=1}^{N} \left[ y_i \log(\hat{y}_i) + (1 - y_i) \log(1 - \hat{y}_i) \right] \]

Why this?

- If true label is 1 and we predict 1: \(-\log(1) = 0\) (no penalty) ✓

- If true label is 1 and we predict 0.01: \(-\log(0.01) \approx 4.6\) (big penalty!) ✓

- Works with probability outputs from sigmoid

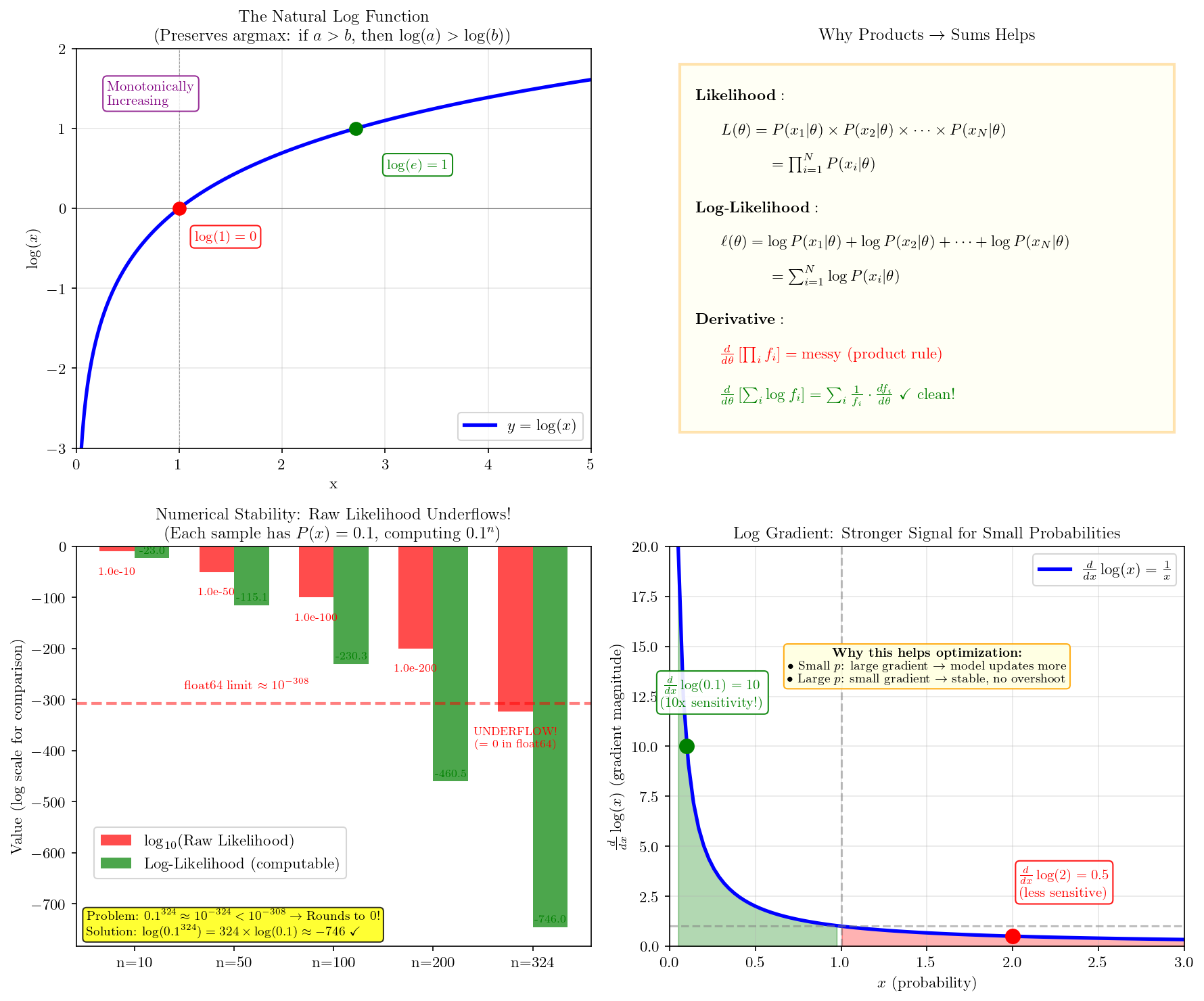

Deriving Cross-Entropy from Maximum Likelihood

The cross-entropy loss isn’t arbitrary—it comes directly from Maximum Likelihood Estimation (MLE). Understanding this derivation reveals why cross-entropy is the natural loss for classification.

Step 1: Model the output as a probability

In logistic regression, we model the probability that \(y = 1\) given input \(x\):

\[P(y = 1 | x) = \hat{y} = \sigma(w^\top x + b)\]

This means \(P(y = 0 | x) = 1 - \hat{y}\).

Step 2: Write the likelihood of one data point

For a single example \((x_i, y_i)\) where \(y_i \in \{0, 1\}\):

\[P(y_i | x_i) = \hat{y}_i^{y_i} \cdot (1 - \hat{y}_i)^{1 - y_i}\]

This elegant formula works because:

- If \(y_i = 1\): \(P = \hat{y}_i^1 \cdot (1 - \hat{y}_i)^0 = \hat{y}_i\) ✓

- If \(y_i = 0\): \(P = \hat{y}_i^0 \cdot (1 - \hat{y}_i)^1 = 1 - \hat{y}_i\) ✓

Step 3: Write the likelihood of all data (assuming independence)

\[\mathcal{L}(w, b) = \prod_{i=1}^{N} P(y_i | x_i) = \prod_{i=1}^{N} \hat{y}_i^{y_i} \cdot (1 - \hat{y}_i)^{1 - y_i}\]

Step 4: Take the log (log-likelihood)

Products are numerically unstable and hard to optimize. Taking the log converts products to sums:

\[\log \mathcal{L} = \sum_{i=1}^{N} \left[ y_i \log(\hat{y}_i) + (1 - y_i) \log(1 - \hat{y}_i) \right]\]

Step 5: Maximize log-likelihood = Minimize negative log-likelihood

We want to maximize the likelihood, but optimizers minimize. So we minimize the negative log-likelihood (NLL):

\[\text{NLL} = -\log \mathcal{L} = -\sum_{i=1}^{N} \left[ y_i \log(\hat{y}_i) + (1 - y_i) \log(1 - \hat{y}_i) \right]\]

Dividing by \(N\) for the average gives us exactly the binary cross-entropy loss!

\[\boxed{\text{BCE} = -\frac{1}{N}\sum_{i=1}^{N} \left[ y_i \log(\hat{y}_i) + (1 - y_i) \log(1 - \hat{y}_i) \right]}\]

Key insight: Cross-entropy is the principled loss for classification because it directly maximizes the probability of the correct labels under our model. This connection to MLE also explains:

- Why it gives clean gradients: \(\frac{\partial \text{BCE}}{\partial z} = \hat{y} - y\)

- Why it’s related to information theory: \(\text{BCE}(p, q) = H(p) + D_{KL}(p || q)\)

- Why it’s the natural choice for probabilistic outputs

Gradient for Logistic Regression

The gradient has a beautiful form:

\[ \frac{\partial \text{Loss}}{\partial w} = \frac{1}{N} \sum_{i=1}^{N} (\hat{y}_i - y_i) x_i \]

Just the error times the input — same form as linear regression!

Note: This gradient computes the average over all examples in the batch:

dw = X.T @ error / len(y). The division bylen(y)ensures the gradient magnitude doesn’t depend on batch size.

Python Implementation

import numpy as np

def sigmoid(z):

return 1 / (1 + np.exp(-z))

# Data: [contains_FREE, contains_!, has_link]

X = np.array([[1, 1, 1],

[0, 0, 0],

[1, 1, 0],

[0, 1, 1],

[1, 0, 1]])

y = np.array([1, 0, 1, 0, 1])

# Initialize

w = np.zeros(3)

b = 0.0

lr = 0.5

for step in range(1000):

# Forward pass

z = X @ w + b

y_pred = sigmoid(z)

# Loss (cross-entropy)

eps = 1e-15 # avoid log(0)

loss = -np.mean(y * np.log(y_pred + eps) + (1 - y) * np.log(1 - y_pred + eps))

# Gradients

error = y_pred - y

dw = X.T @ error / len(y)

db = np.mean(error)

# Update

w = w - lr * dw

b = b - lr * db

if step % 200 == 0:

predictions = (y_pred > 0.5).astype(int)

accuracy = np.mean(predictions == y)

print(f"Step {step}: loss={loss:.4f}, accuracy={accuracy:.0%}")

# Final: w=[1.23, 0.41, 0.41], b=-0.82, accuracy=100%1.5 Multi-Layer Perceptron (MLP)

Limitation of Linear Models

Linear and logistic regression can only learn linear decision boundaries:

Linearly separable: NOT separable (XOR):

x₂↑ x₂↑

| + + + | - +

| + + + |

----+--------→ x₁ -----+-----→ x₁

| - - - |

| - - | + -To learn complex patterns, we need non-linear models.

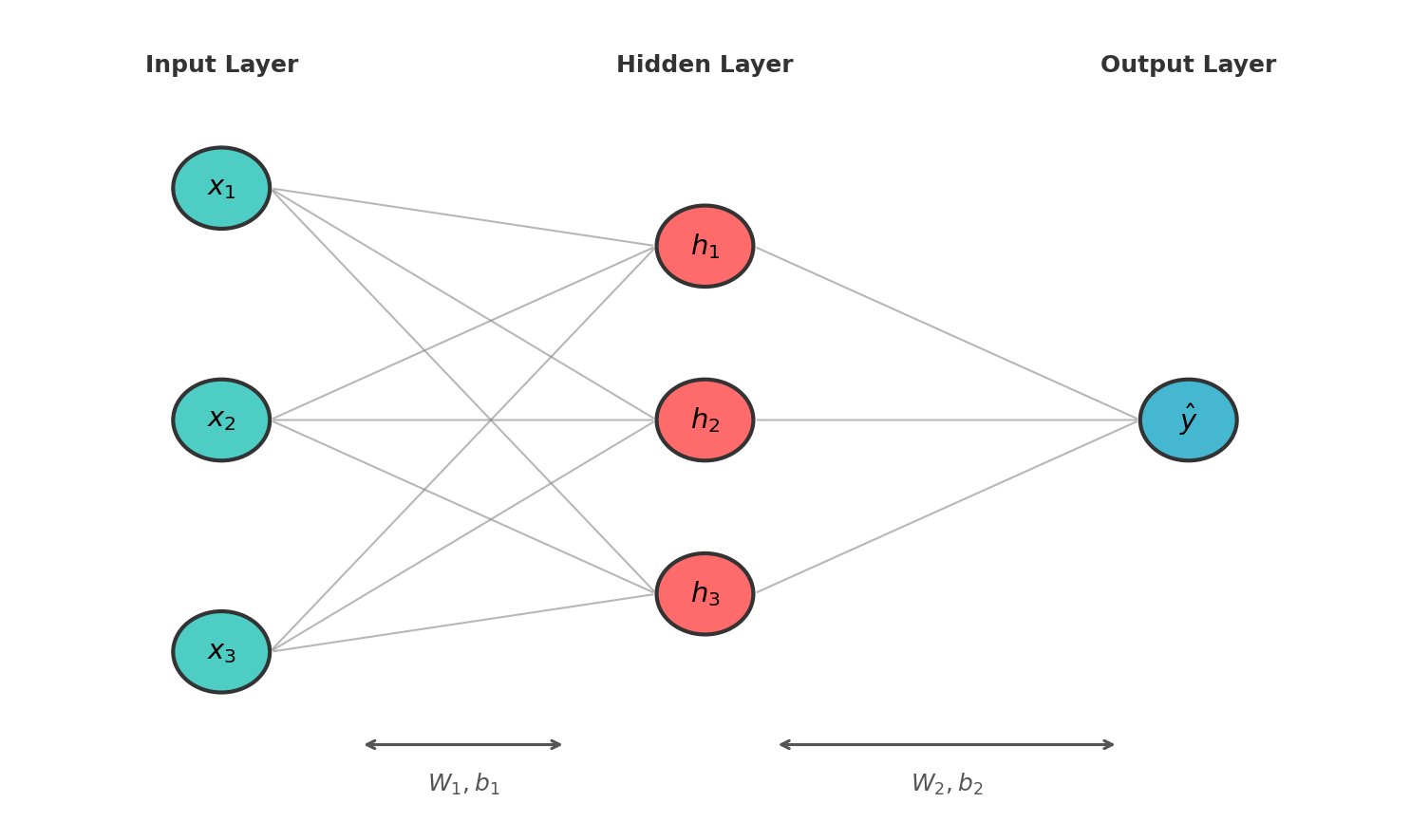

The MLP: Stacking Layers

An MLP adds hidden layers between input and output:

Figure: Multi-layer perceptron

with input layer, hidden layer, and output layer. Each

connection represents a weight.

Figure: Multi-layer perceptron

with input layer, hidden layer, and output layer. Each

connection represents a weight.

Forward Pass (Step by Step)

For a network with one hidden layer:

Layer 1: Linear transformation + activation \[ z_1 = W_1 x + b_1 \]

\[ h = \text{ReLU}(z_1) = \max(0, z_1) \]

Layer 2: Another linear transformation \[ z_2 = W_2 h + b_2 \]

\[ \hat{y} = \text{softmax}(z_2) \quad \text{(for classification)} \]

Activation Functions: Why We Need Them

Without activation functions, stacking linear layers is useless:

\[ W_2(W_1 x + b_1) + b_2 = W_2 W_1 x + W_2 b_1 + b_2 = W' x + b' \]

Still linear! Activation functions introduce non-linearity.

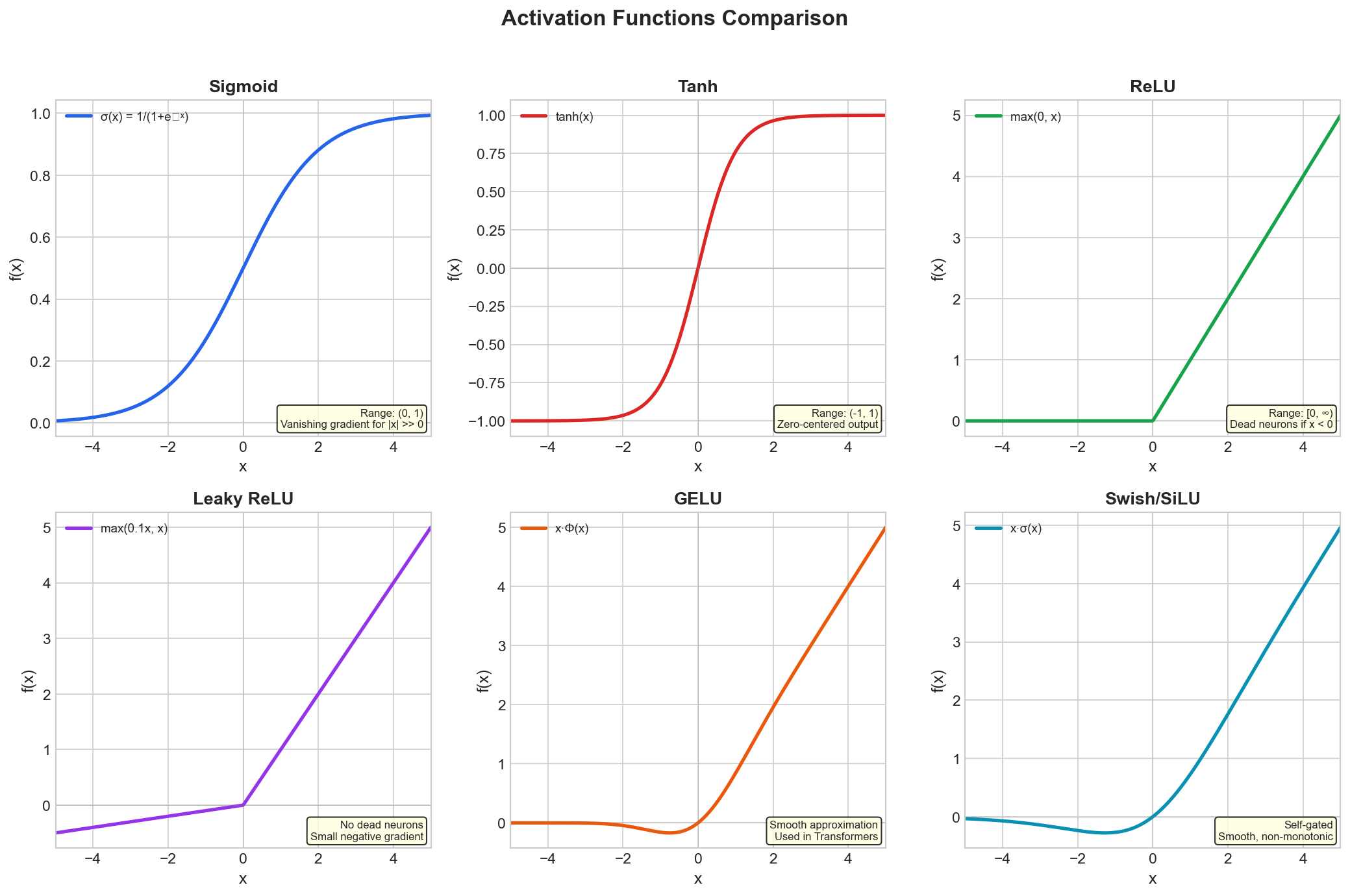

Common Activation Functions

| Function | Formula | Range | Used For |

|---|---|---|---|

| Sigmoid | \(\frac{1}{1+e^{-x}}\) | \((0, 1)\) | Binary classification output |

| Tanh | \(\frac{e^x - e^{-x}}{e^x + e^{-x}}\) | \((-1, 1)\) | Hidden layers (older) |

| ReLU | \(\max(0, x)\) | \([0, \infty)\) | Hidden layers (modern default) |

| Softmax | \(\frac{e^{x_i}}{\sum_j e^{x_j}}\) | \((0, 1)\), sums to 1 | Multi-class output |

Figure: Common activation

functions including ReLU, Sigmoid, Tanh, and their

variants.

Figure: Common activation

functions including ReLU, Sigmoid, Tanh, and their

variants.

ReLU: Why It Works

- Simple: Fast to compute

- Sparse: Many neurons output 0 (efficient)

- No vanishing gradient: Gradient is 1 for positive inputs

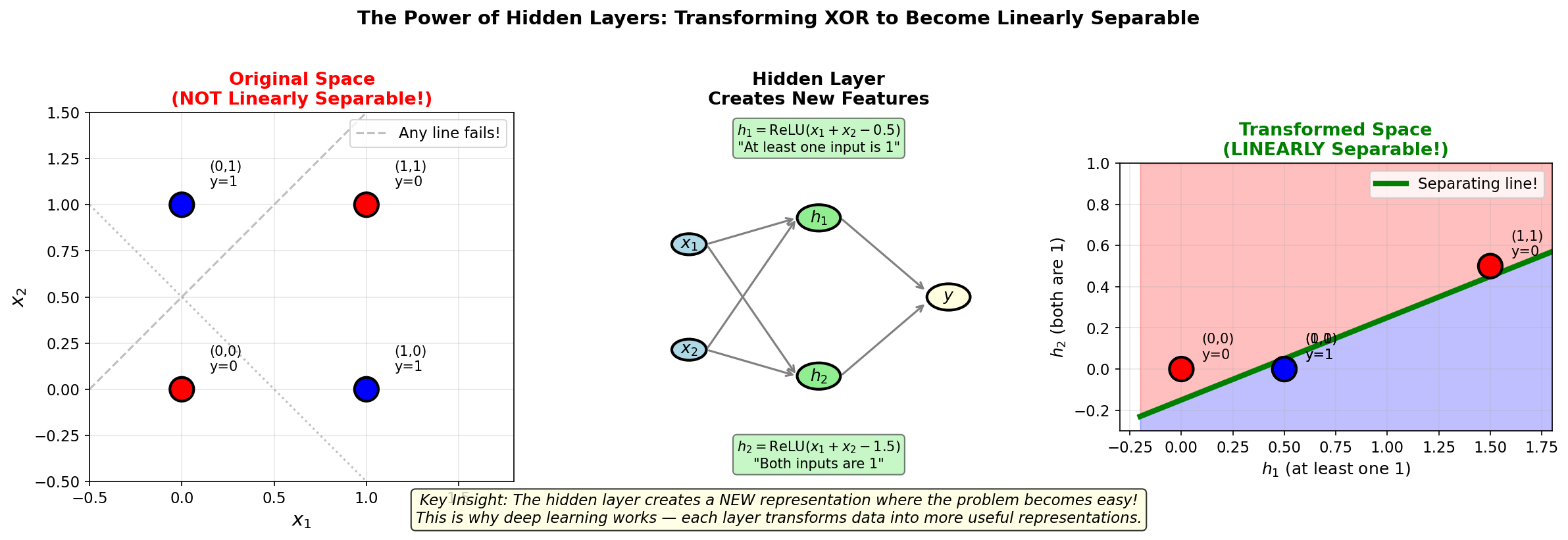

Concrete Example: Learning XOR

XOR function:

| \(x_1\) | \(x_2\) | XOR |

|---|---|---|

| 0 | 0 | 0 |

| 0 | 1 | 1 |

| 1 | 0 | 1 |

| 1 | 1 | 0 |

No line can separate 0s from 1s!

MLP Solution

Hidden layer (2 neurons): \[ h_1 = \text{ReLU}(x_1 + x_2 - 0.5) \quad \text{(detects "at least one 1")} \]

\[ h_2 = \text{ReLU}(x_1 + x_2 - 1.5) \quad \text{(detects "both are 1")} \]

Output: \[ \hat{y} = h_1 - 2 \cdot h_2 \]

| \(x_1\) | \(x_2\) | \(h_1\) | \(h_2\) | \(\hat{y}\) |

|---|---|---|---|---|

| 0 | 0 | 0 | 0 | 0 |

| 0 | 1 | 0.5 | 0 | 0.5 → 1 |

| 1 | 0 | 0.5 | 0 | 0.5 → 1 |

| 1 | 1 | 1 | 0.5 | 0 → 0 |

The hidden layer creates a new representation where the problem becomes linearly separable!

Figure: The power of hidden

layers. Left: In the original input space, XOR is NOT

linearly separable — no single line can separate the red

class (0) from the blue class (1). Middle: The hidden layer

computes new features \(h_1\) (“at least one 1”) and

\(h_2\) (“both are 1”).

Right: In the transformed space, the problem becomes

linearly separable! This is the key insight behind deep

learning: each layer transforms data into more useful

representations.

Figure: The power of hidden

layers. Left: In the original input space, XOR is NOT

linearly separable — no single line can separate the red

class (0) from the blue class (1). Middle: The hidden layer

computes new features \(h_1\) (“at least one 1”) and

\(h_2\) (“both are 1”).

Right: In the transformed space, the problem becomes

linearly separable! This is the key insight behind deep

learning: each layer transforms data into more useful

representations.

Python Implementation

import numpy as np

def relu(x):

return np.maximum(0, x)

def relu_derivative(x):

return (x > 0).astype(float)

def sigmoid(x):

return 1 / (1 + np.exp(-x))

# XOR data

X = np.array([[0, 0], [0, 1], [1, 0], [1, 1]])

y = np.array([[0], [1], [1], [0]])

# Network: 2 inputs → 4 hidden → 1 output

np.random.seed(42)

W1 = np.random.randn(2, 4) * 0.5

b1 = np.zeros((1, 4))

W2 = np.random.randn(4, 1) * 0.5

b2 = np.zeros((1, 1))

lr = 1.0

for step in range(10000):

# Forward pass

z1 = X @ W1 + b1

h = relu(z1)

z2 = h @ W2 + b2

y_pred = sigmoid(z2)

# Loss

loss = np.mean((y - y_pred) ** 2)

# Backward pass (will explain in next section!)

d_z2 = (y_pred - y) * y_pred * (1 - y_pred)

d_W2 = h.T @ d_z2

d_b2 = np.sum(d_z2, axis=0, keepdims=True)

d_h = d_z2 @ W2.T

d_z1 = d_h * relu_derivative(z1)

d_W1 = X.T @ d_z1

d_b1 = np.sum(d_z1, axis=0, keepdims=True)

# Update

W2 -= lr * d_W2

b2 -= lr * d_b2

W1 -= lr * d_W1

b1 -= lr * d_b1

if step % 1000 == 0:

print(f"Step {step}: loss={loss:.4f}")

# Test

print("\nPredictions:")

print(np.round(y_pred, 2))

# [[0.02], [0.98], [0.98], [0.02]] ✓1.6 The Backpropagation Algorithm

The Problem: How to Get Gradients in Deep Networks?

For linear regression: straightforward calculus.

For deep networks with millions of parameters: we need an efficient algorithm.

Backpropagation = Backward propagation of errors

The Chain Rule: The Key Insight

If \(y = f(g(x))\), then:

\[ \frac{dy}{dx} = \frac{dy}{dg} \cdot \frac{dg}{dx} \]

In neural networks, we have a chain of operations:

\[ x \to z_1 \to h \to z_2 \to \hat{y} \to \text{Loss} \]

To find \(\frac{\partial \text{Loss}}{\partial W_1}\), we apply the chain rule through each step.

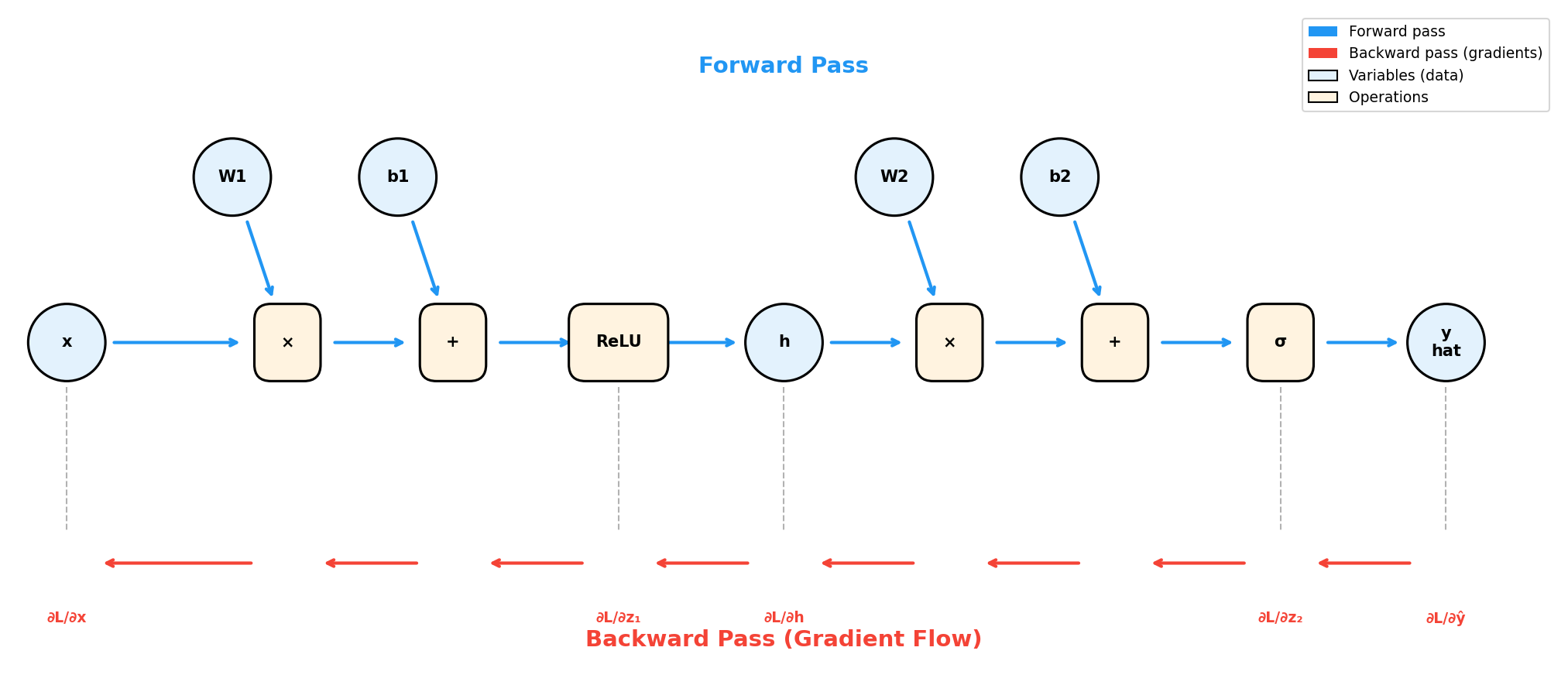

Visualizing Backpropagation: The Computational Graph

A computational graph makes backpropagation intuitive. Each node represents either a variable (data) or an operation. Edges show data flow.

Figure: A computational

graph for a 2-layer MLP. Blue arrows show forward pass (data

flowing left to right). Red arrows show backward pass

(gradients flowing right to left). Each operation node

computes a “local gradient” that gets multiplied along the

path.

Figure: A computational

graph for a 2-layer MLP. Blue arrows show forward pass (data

flowing left to right). Red arrows show backward pass

(gradients flowing right to left). Each operation node

computes a “local gradient” that gets multiplied along the

path.

Key insight: During backprop, we traverse the same graph in reverse, multiplying local gradients along each path.

The algorithm:

- Forward pass: Compute all intermediate values, storing them for later

- Backward pass: Starting from the loss,

compute gradients by:

- For each operation node, multiply the incoming gradient by the local gradient

- Sum gradients when paths merge (multiple outputs from one node)

Example with specific values:

Forward: x=2 → [×W₁=3] → z₁=6 → [ReLU] → h=6 → [×W₂=0.5] → z₂=3 → [σ] → ŷ=0.95

If y=1: Loss = -log(0.95) = 0.05

Backward:

∂L/∂ŷ = -1/0.95 = -1.05

∂L/∂z₂ = -1.05 × σ'(3) = -1.05 × 0.95 × 0.05 = -0.05

∂L/∂W₂ = -0.05 × h = -0.05 × 6 = -0.30

∂L/∂h = -0.05 × W₂ = -0.05 × 0.5 = -0.025

∂L/∂z₁ = -0.025 × 1 (ReLU'=1 since z₁>0) = -0.025

∂L/∂W₁ = -0.025 × x = -0.025 × 2 = -0.05Why computational graphs matter: - Automatic differentiation frameworks (PyTorch, TensorFlow) build these graphs automatically - Any differentiable computation can be expressed as a graph - Backprop becomes mechanical: just apply the chain rule at each node

Backprop: Step by Step

Consider our 2-layer MLP:

Forward pass (compute and cache everything):

z₁ = W₁x + b₁

h = ReLU(z₁)

z₂ = W₂h + b₂

ŷ = sigmoid(z₂)

L = MSE(y, ŷ)Backward pass (work backwards from loss):

Gradient of loss w.r.t. output: \[ \frac{\partial L}{\partial \hat{y}} = \hat{y} - y \]

Through sigmoid: The sigmoid derivative has an elegant form. Starting from \(\sigma(z) = \frac{1}{1+e^{-z}}\):

\[\sigma'(z) = \frac{d}{dz}\frac{1}{1+e^{-z}} = \frac{e^{-z}}{(1+e^{-z})^2} = \frac{1}{1+e^{-z}} \cdot \frac{e^{-z}}{1+e^{-z}} = \sigma(z)(1-\sigma(z))\]

Therefore: \[ \frac{\partial L}{\partial z_2} = \frac{\partial L}{\partial \hat{y}} \cdot \sigma'(z_2) = (\hat{y} - y) \cdot \hat{y}(1 - \hat{y}) \]

Gradient for \(W_2\): \[ \frac{\partial L}{\partial W_2} = h^\top \cdot \frac{\partial L}{\partial z_2} \]

Propagate to hidden layer: \[ \frac{\partial L}{\partial h} = \frac{\partial L}{\partial z_2} \cdot W_2^\top \]

Through ReLU: \[ \frac{\partial L}{\partial z_1} = \frac{\partial L}{\partial h} \cdot \mathbf{1}_{z_1 > 0} \]

Gradient for \(W_1\): \[ \frac{\partial L}{\partial W_1} = x^\top \cdot \frac{\partial L}{\partial z_1} \]

Why It’s Efficient

- Forward pass: \(O(\text{network size})\) — just matrix multiplications

- Backward pass: \(O(\text{network size})\) — same complexity as forward!

- Total: \(O(\text{network size})\) per example

Without backprop, computing each parameter’s gradient separately would be \(O((\text{network size})^2)\).

Automatic Differentiation

Modern frameworks (PyTorch, TensorFlow) implement backprop automatically:

import torch

import torch.nn as nn

# Define network

model = nn.Sequential(

nn.Linear(2, 4),

nn.ReLU(),

nn.Linear(4, 1),

nn.Sigmoid()

)

# Training

X = torch.tensor([[0, 0], [0, 1], [1, 0], [1, 1]], dtype=torch.float32)

y = torch.tensor([[0], [1], [1], [0]], dtype=torch.float32)

optimizer = torch.optim.SGD(model.parameters(), lr=1.0)

loss_fn = nn.MSELoss()

for step in range(10000):

# Forward

y_pred = model(X)

loss = loss_fn(y_pred, y)

# Backward (automatically computes all gradients!)

optimizer.zero_grad()

loss.backward()

# Update

optimizer.step()

if step % 1000 == 0:

print(f"Step {step}: loss={loss.item():.4f}")1.7 Softmax and Multi-class Classification

From Binary to Multi-class

Logistic regression handles 2 classes. For K classes, we use softmax:

\[P(y = k | x) = \frac{e^{z_k}}{\sum_{j=1}^{K} e^{z_j}}\]

where \(z_k = w_k \cdot x + b_k\) is the logit for class \(k\).

Properties of Softmax

- Outputs sum to 1: \(\sum_k P(y = k | x) = 1\) ✓

- All outputs positive: \(P(y = k | x) > 0\) ✓

- Preserves ranking: Largest logit → highest probability

Why Exponential (Not Simple Normalization)?

Interview Question: “Why does softmax use \(e^{z_i}\) instead of just \(\frac{z_i}{\sum_j z_j}\)?”

Simple normalization would be: \(\text{normalize}(z_i) = \frac{z_i}{\sum_j z_j}\)

This fails for several critical reasons:

Problem 1: Negative Values Break Everything

Logits: [2, -3, 1]

Sum = 0 → Division by zero!

Logits: [2, -5, 1]

Sum = -2

"Probabilities": [2/-2, -5/-2, 1/-2] = [-1, 2.5, -0.5]

→ Negative "probabilities"! Invalid!Exponentials are always positive: \(e^x > 0\) for all \(x\), so softmax outputs are always valid probabilities.

Problem 2: Beautiful Gradient Properties

The softmax + cross-entropy gradient has an elegant form:

\[\frac{\partial L}{\partial z_i} = p_i - y_i\]

where \(p_i\) is predicted probability and \(y_i\) is the target (1 for correct class, 0 otherwise).

This clean gradient comes directly from the exponential. Simple normalization would give messier, harder-to-optimize gradients.

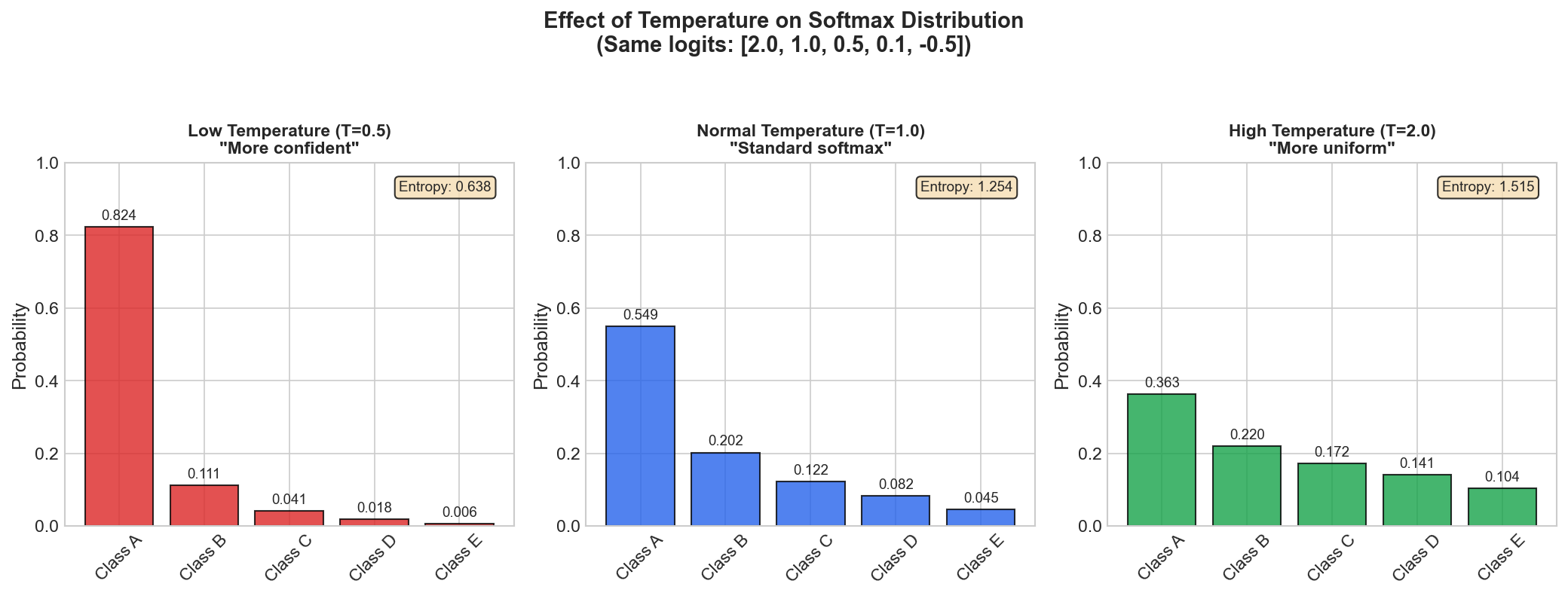

Problem 3: Amplification with Temperature Control

Exponentials amplify differences between logits:

Logits: [2.0, 1.0, 0.5]

Simple normalize: [2/3.5, 1/3.5, 0.5/3.5] = [0.57, 0.29, 0.14]

Softmax: [0.59, 0.24, 0.17] # Winner amplifiedTemperature provides explicit control over this amplification:

\[\text{softmax}(z_i / T) = \frac{e^{z_i/T}}{\sum_j e^{z_j/T}}\]

- \(T \to 0\): Approaches argmax (one-hot, hard selection)

- \(T = 1\): Standard softmax

- \(T \to \infty\): Approaches uniform distribution

This is used in knowledge distillation (soft targets) and sampling diversity control.

Problem 4: Theoretical Grounding (Maximum Entropy)

Softmax is the maximum entropy distribution subject to linear constraints on expected features. This connects to:

- Statistical mechanics (Boltzmann distribution)

- Information theory (exponential family distributions)

- Principled probabilistic modeling

Summary: Exponentials ensure:

- ✅ Always positive outputs (valid probabilities)

- ✅ Sum to 1 (proper distribution)

- ✅ Clean gradients for efficient learning

- ✅ Controllable sharpness via temperature

- ✅ Theoretically principled (max entropy)

Example: 3-Class Classification

Input x → [Linear Layer] → Logits z → [Softmax] → Probabilities

z = [2.0, 1.0, 0.1]

softmax(z):

e^2.0 = 7.39

e^1.0 = 2.72

e^0.1 = 1.11

sum = 11.22

P = [7.39/11.22, 2.72/11.22, 1.11/11.22]

= [0.66, 0.24, 0.10] Figure: Effect of

temperature on softmax distribution. Lower temperature makes

the distribution sharper (more confident), higher

temperature makes it more uniform.

Figure: Effect of

temperature on softmax distribution. Lower temperature makes

the distribution sharper (more confident), higher

temperature makes it more uniform.

Multi-class Cross-Entropy Loss

For one-hot label \(y\) (e.g., \(y = [0, 1, 0]\) for class 2):

\[\mathcal{L} = -\sum_{k=1}^{K} y_k \log(\hat{y}_k) = -\log(\hat{y}_c)\]

where \(c\) is the true class. We’re penalizing low probability on the correct class.

PyTorch Implementation

import torch.nn as nn

# Method 1: Separate softmax and loss

probs = nn.Softmax(dim=1)(logits)

loss = nn.NLLLoss()(torch.log(probs), labels)

# Method 2: Combined (numerically stable, preferred!)

loss = nn.CrossEntropyLoss()(logits, labels) # Takes raw logits!⚠️ Common mistake:

CrossEntropyLoss expects

logits, not probabilities!

1.8 Batching: Why and How

What This Means (For Beginners)

When training a neural network, three terms come up constantly: Epoch, Batch, and Iteration. Understanding how they relate is fundamental.

Epoch = One complete pass through the entire training dataset

Think of studying for an exam: - 1 epoch: You go through the entire syllabus once - 5 epochs: You study the same syllabus five times, each time understanding more

Batch = A subset of the training data processed together

Since the entire dataset is often too large to fit in GPU memory at once, we divide it into smaller chunks called batches. Each batch is processed in one forward pass and one backward pass.

Iteration = One forward + backward pass on one batch

Each iteration updates the model’s weights once.

The Key Formula

\[\text{Iterations per epoch} = \frac{\text{Total training samples}}{\text{Batch size}}\]

Worked Example

Suppose you have 1,000 training samples and set batch size = 100:

Total samples: 1,000

Batch size: 100

Iterations/epoch: 1,000 / 100 = 10

What happens in 1 epoch:

Iteration 1: Process samples 1-100 → Update weights

Iteration 2: Process samples 101-200 → Update weights

Iteration 3: Process samples 201-300 → Update weights

...

Iteration 10: Process samples 901-1000 → Update weights

After 10 iterations, you've completed 1 epoch!For 3 epochs with batch_size=100 on 1,000 samples: - Total iterations = 3 epochs × 10 iterations/epoch = 30 weight updates - Each sample is seen 3 times total (once per epoch)

Visual Summary

┌────────────────────────────────────────────────────────────────┐

│ FULL DATASET (1000 samples) │

├─────────┬─────────┬─────────┬─────────┬───────────┬────────────┤

│ Batch 1 │ Batch 2 │ Batch 3 │ Batch 4 │ ... │ Batch 10 │

│ (100) │ (100) │ (100) │ (100) │ │ (100) │

└─────────┴─────────┴─────────┴─────────┴───────────┴────────────┘

↓ ↓ ↓ ↓ ↓

Iter 1 Iter 2 Iter 3 Iter 4 ... Iter 10

└──────────────────────┬──────────────────────────┘

│

= 1 EPOCHThe Pizza Analogy 🍕

- The entire pizza = Full training dataset

- Each slice = One batch

- Eating one slice = One iteration (process one batch, update weights)

- Finishing the whole pizza = One epoch (processed all samples once)

If the pizza has 8 slices and you eat 1 slice at a time: - You need 8 iterations to finish 1 pizza (1 epoch) - Training for 3 epochs = eating 3 pizzas = 24 slices eaten = 24 iterations

Why Multiple Epochs?

Training for a single epoch usually isn’t enough: - The model makes one pass through each sample - Weights are updated based on each batch, but may not have converged - By repeating for multiple epochs, the model gradually refines its understanding

Epoch 1: Model learns rough patterns

Epoch 2: Model refines understanding

Epoch 3: Model fine-tunes details

...

Epoch N: Model converges (loss stops decreasing)Warning: Too many epochs can lead to overfitting! The model memorizes the training data instead of learning generalizable patterns. This is why we monitor validation loss.

Interview Q: “What’s the difference between epoch, batch, and iteration?”

A: An epoch is one complete pass through the entire training dataset. A batch is a subset of the data processed together in one forward/backward pass. An iteration is one weight update, which happens after processing one batch.

The relationship:

Iterations per epoch = Dataset size / Batch size

For example, with 10,000 samples and batch size 100, you have 100 iterations per epoch. Training for 5 epochs means 500 total weight updates, with each sample seen 5 times.

The Problem with Single Examples

Computing gradient on one example at a time:

- Very noisy updates

- Can’t utilize GPU parallelism

- Slow convergence

Computing gradient on entire dataset:

- Very stable but slow

- One update per epoch

- Memory can’t hold all data

Mini-batch: The Sweet Spot

Dataset: 10,000 examples

Batch size: 32

→ 10,000 / 32 = 312 batches per epoch

→ 312 gradient updates per epochWhy Batching Works

The mini-batch gradient is an unbiased estimator of the full gradient:

\[\mathbb{E}\left[\frac{1}{B}\sum_{i \in \text{batch}} \nabla \ell_i\right] = \frac{1}{N}\sum_{i=1}^{N} \nabla \ell_i\]

Batch Size Tradeoffs

| Small Batch (32) | Large Batch (4096) |

|---|---|

| High variance (noisy) | Low variance (stable) |

| Good generalization | May generalize worse |

| More updates per epoch | Fewer updates |

| Slower per update | Faster per update (GPU) |

| Works on any GPU | Needs large GPU memory |

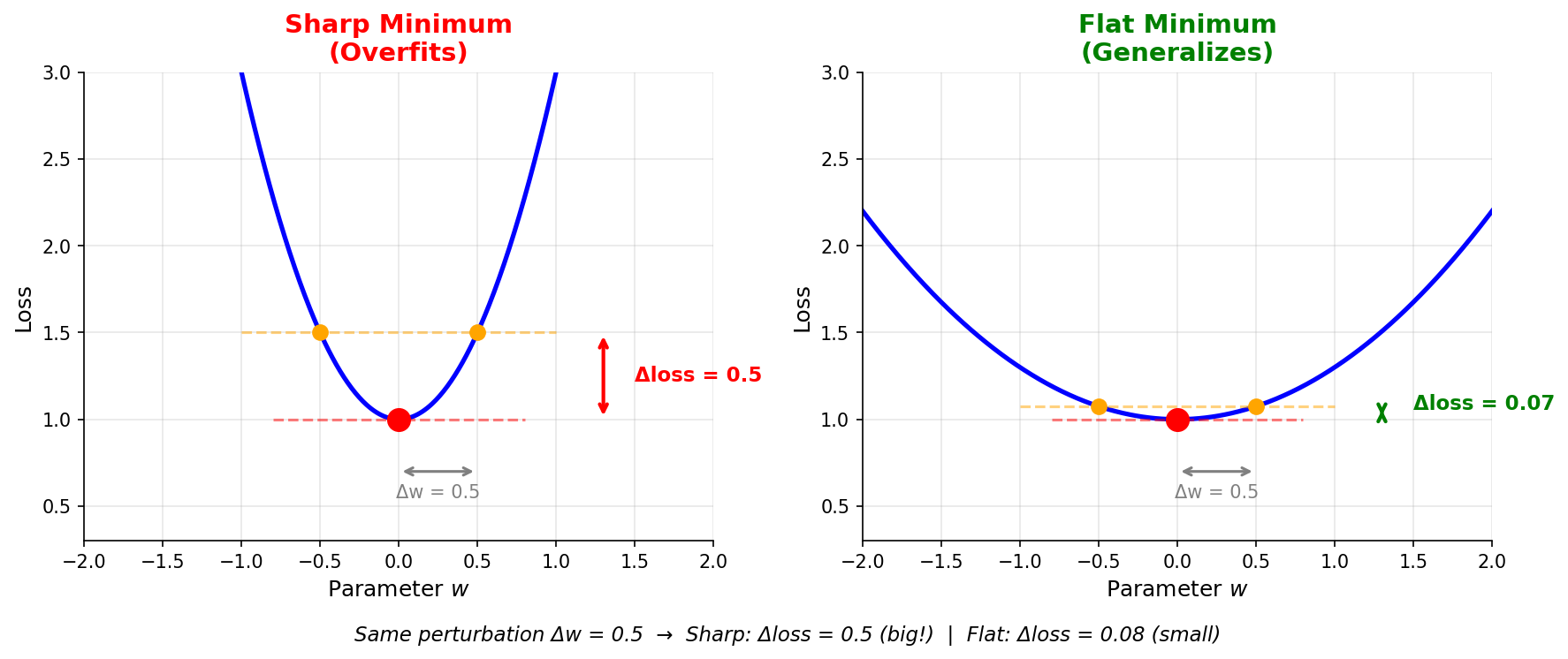

The “Noise is Good” Insight

Small batch noise acts as implicit regularization:

- Helps escape sharp minima (which generalize poorly)

- Finds flatter minima (which generalize better)

Figure: Sharp minima

(left) overfit because small weight changes cause large loss

changes. Flat minima (right) generalize better because

they’re robust to perturbations.

Figure: Sharp minima

(left) overfit because small weight changes cause large loss

changes. Flat minima (right) generalize better because

they’re robust to perturbations.

Practical Guidelines

| Dataset Size | Typical Batch Size |

|---|---|

| < 1,000 | 8-32 |

| 1,000-100,000 | 32-128 |

| > 100,000 | 128-512 |

| LLM pretraining | 1M-4M tokens |

Code Example: Batching in PyTorch

from torch.utils.data import DataLoader, TensorDataset

# Create dataset and loader

dataset = TensorDataset(X_tensor, y_tensor)

loader = DataLoader(dataset, batch_size=32, shuffle=True)

# Training loop

for epoch in range(num_epochs):

for batch_X, batch_y in loader:

# Forward pass on batch

predictions = model(batch_X)

loss = criterion(predictions, batch_y)

# Backward pass

optimizer.zero_grad()

loss.backward()

optimizer.step()1.9 Data Preprocessing

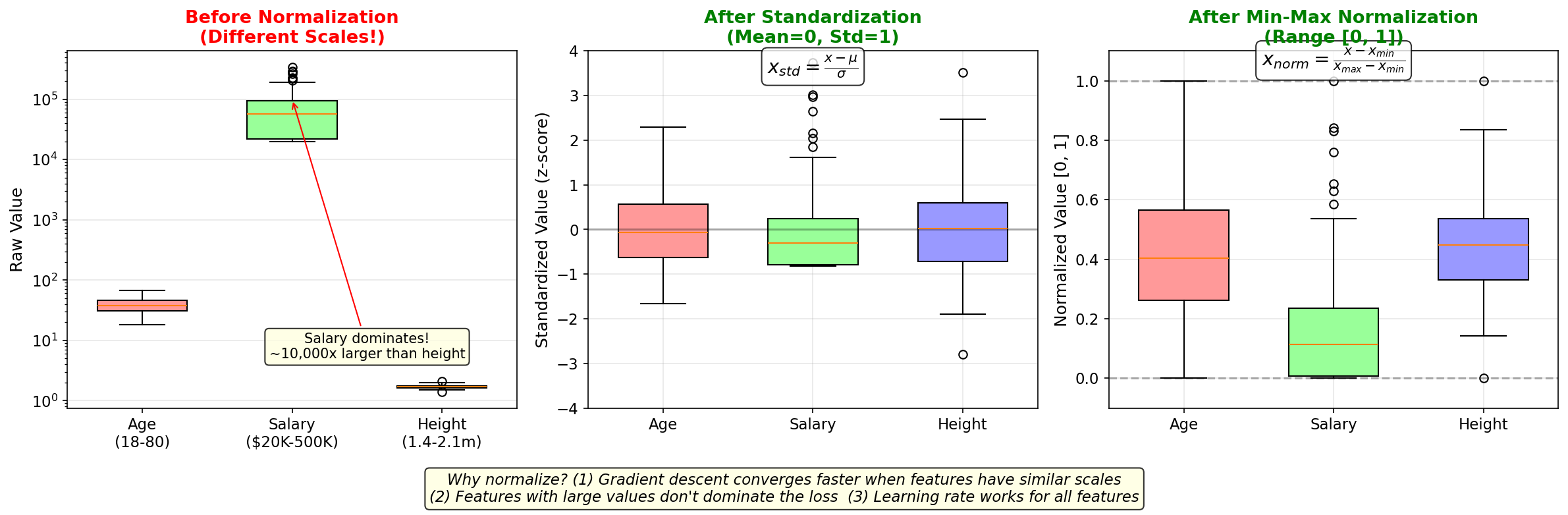

Why Preprocess?

Raw features often have different scales:

- Age: 0-100

- Salary: 20,000-500,000

- Height: 1.5-2.0 meters

Without preprocessing:

- Large-scale features dominate gradients

- Small learning rates needed for some features

- Optimization is slow and unstable

Standardization (Z-score Normalization)

\[x' = \frac{x - \mu}{\sigma}\]

Result: Mean = 0, Std = 1

# Training set

mean = X_train.mean(axis=0)

std = X_train.std(axis=0)

# Apply to all sets using TRAINING statistics!

X_train_scaled = (X_train - mean) / std

X_test_scaled = (X_test - mean) / std # Same mean/std!⚠️ Critical: Always compute statistics on training data only, then apply to test data!

Min-Max Normalization

\[x' = \frac{x - x_{\min}}{x_{\max} - x_{\min}}\]

Result: Range [0, 1]

Figure: Why preprocessing

matters. Left: Raw features at vastly different scales —

salary dominates (10,000× larger than height). Middle: After

standardization (z-score), all features have mean=0 and

std=1. Right: After min-max normalization, all features are

in [0, 1]. Without normalization, gradient descent would be

dominated by large-scale features.

Figure: Why preprocessing

matters. Left: Raw features at vastly different scales —

salary dominates (10,000× larger than height). Middle: After

standardization (z-score), all features have mean=0 and

std=1. Right: After min-max normalization, all features are

in [0, 1]. Without normalization, gradient descent would be

dominated by large-scale features.

When to Use Which?

| Method | When to Use |

|---|---|

| Standardization | Most cases; neural networks; data has outliers |

| Min-Max | Need bounded range; image pixels (0-255 → 0-1) |

| No preprocessing | Tree-based models (don’t need it) |

Image Preprocessing

# Typical ImageNet preprocessing

transform = transforms.Compose([

transforms.Resize(256),

transforms.CenterCrop(224),

transforms.ToTensor(), # Converts to [0, 1]

transforms.Normalize(

mean=[0.485, 0.456, 0.406], # ImageNet stats

std=[0.229, 0.224, 0.225]

)

])Text Preprocessing

- Tokenization: “Hello world” → [“Hello”, “world”] → [15496, 995]

- Padding: Make all sequences same length

- Embedding: Token IDs → dense vectors

Handling Missing Values

Real-world datasets often have missing values. Understanding why data is missing guides how to handle it.

Types of Missingness:

| Type | Abbreviation | Meaning | Example |

|---|---|---|---|

| Missing Completely at Random | MCAR | Missingness is unrelated to any variable | Survey respondent accidentally skipped a question |

| Missing at Random | MAR | Missingness depends on observed variables | Younger people less likely to report income (but we know their age) |

| Missing Not at Random | MNAR | Missingness depends on the missing value itself | High earners don’t report income because it’s high |

Why It Matters: MCAR is “safe” — any handling method works. MAR can be handled with imputation if you model the missingness. MNAR is problematic — you can’t fully correct for it without additional information.

Handling Strategies:

| Strategy | Method | When to Use | Drawback |

|---|---|---|---|

| Deletion | Drop rows with missing values | MCAR + few missing values (<5%) | Loses data, can bias if not MCAR |

| Mean/Median Imputation | Replace with column mean/median | Numerical features, MCAR | Reduces variance, ignores relationships |

| Mode Imputation | Replace with most frequent value | Categorical features | Over-represents common values |

| KNN Imputation | Use K-nearest neighbors to estimate | MAR, when features are correlated | Computationally expensive |

| Model-based | Train model to predict missing values | MAR, large datasets | Can propagate errors |

| Indicator Variable | Add binary “was_missing” column | When missingness itself is informative | Increases dimensionality |

⚠️ Important: Imputation Considerations

Imputation means filling in missing values with estimated values. Key points:

- Imputation introduces bias: The imputed values are estimates, not real data. They reduce variance and can make relationships appear stronger than they are.

- Never impute the target variable: If your label/outcome is missing, that sample should typically be excluded, not imputed.

- Fit imputer on training data only: Just like with normalization, compute imputation statistics (mean, median, etc.) on training data, then apply to validation/test sets. This prevents data leakage.

- Consider multiple imputation: For statistical inference, advanced techniques like MICE (Multiple Imputation by Chained Equations) account for uncertainty in imputed values.

- Document your approach: Always report what percentage of data was missing and how you handled it—this affects reproducibility.

Python Examples:

import pandas as pd

import numpy as np

from sklearn.impute import SimpleImputer, KNNImputer

# Sample data with missing values

df = pd.DataFrame({

'age': [25, 30, np.nan, 45, 50],

'income': [50000, np.nan, 70000, 80000, np.nan],

'category': ['A', 'B', np.nan, 'A', 'B']

})

# Method 1: Drop rows with any missing values

df_dropped = df.dropna() # 2 rows remain

# Method 2: Mean imputation for numerical columns

mean_imputer = SimpleImputer(strategy='mean')

df['age_imputed'] = mean_imputer.fit_transform(df[['age']])

# Method 3: Median imputation (robust to outliers)

median_imputer = SimpleImputer(strategy='median')

df['income_imputed'] = median_imputer.fit_transform(df[['income']])

# Method 4: Mode imputation for categorical

mode_imputer = SimpleImputer(strategy='most_frequent')

df['category_imputed'] = mode_imputer.fit_transform(df[['category']])

# Method 5: KNN imputation (considers feature relationships)

knn_imputer = KNNImputer(n_neighbors=2)

numerical_cols = df[['age', 'income']].values

df_knn = pd.DataFrame(knn_imputer.fit_transform(numerical_cols),

columns=['age_knn', 'income_knn'])

# Method 6: Add missingness indicator

df['income_was_missing'] = df['income'].isna().astype(int)Interview Q: “How would you handle missing values in a dataset?”

A: First, I’d analyze the missingness pattern to determine if it’s MCAR, MAR, or MNAR — this guides the approach. For MCAR with few missing values (<5%), simple deletion may work. For numerical features, I’d use median imputation (robust to outliers) or KNN imputation if features are correlated. For categorical features, mode imputation or a separate “Unknown” category. If missingness itself might be informative (e.g., people skip income questions intentionally), I’d add an indicator variable. For MAR in large datasets, model-based imputation (like using Random Forest to predict missing values) can capture complex relationships. I’d always validate by comparing model performance with different imputation strategies.

Outlier Detection and Handling

Interview Q: “How do you detect and handle outliers in your data? How do you make models robust to outliers?”

Outliers are data points that are significantly different from other observations. They can be:

- True outliers: Rare but valid data points (e.g., a billionaire in income data)

- Errors: Data entry mistakes, sensor malfunctions, or corruption

Detection Methods

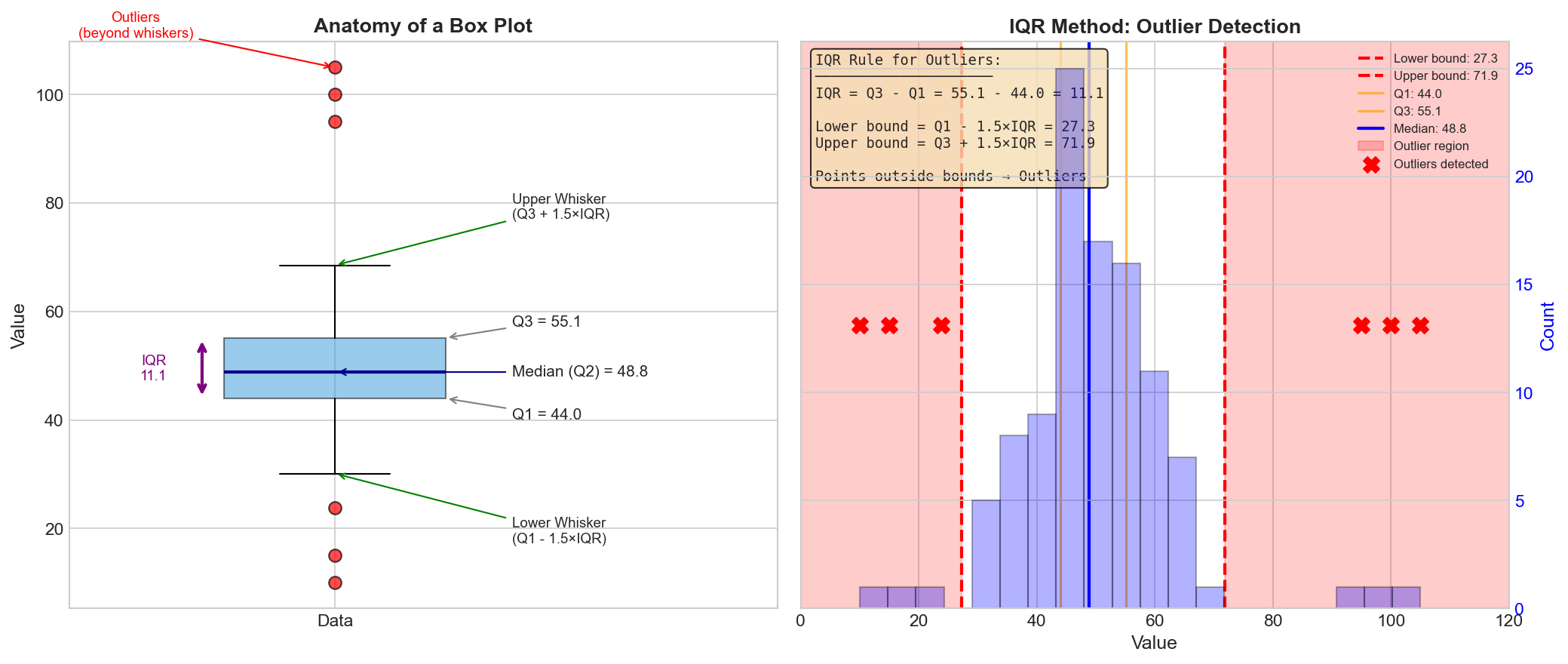

1. Interquartile Range (IQR) Method (Box-Plot/Tukey’s Fences)

The most common statistical method, based on the interquartile range:

IQR = Q3 - Q1

Lower bound = Q1 - 1.5 × IQR

Upper bound = Q3 + 1.5 × IQR

Points outside these bounds → Outliers Figure: Anatomy of a box-plot

(left) showing Q1, median, Q3, IQR, and whiskers. The IQR

method (right) detects outliers as points beyond Q1 -

1.5×IQR or Q3 + 1.5×IQR.

Figure: Anatomy of a box-plot

(left) showing Q1, median, Q3, IQR, and whiskers. The IQR

method (right) detects outliers as points beyond Q1 -

1.5×IQR or Q3 + 1.5×IQR.

import numpy as np

def detect_outliers_iqr(data):

"""Detect outliers using IQR method (1.5×IQR rule)"""

Q1 = np.percentile(data, 25)

Q3 = np.percentile(data, 75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

outliers = (data < lower_bound) | (data > upper_bound)

return outliers, lower_bound, upper_bound

# Example

data = np.array([1, 2, 3, 4, 5, 6, 7, 8, 9, 100]) # 100 is outlier

is_outlier, lb, ub = detect_outliers_iqr(data)

print(f"Outliers: {data[is_outlier]}") # [100]2. Z-Score Method

For normally distributed data, points far from the mean (typically > 3σ) are outliers:

\[z = \frac{x - \mu}{\sigma}\]

def detect_outliers_zscore(data, threshold=3):

"""Detect outliers using Z-score (points > threshold std from mean)"""

mean = np.mean(data)

std = np.std(data)

z_scores = np.abs((data - mean) / std)

return z_scores > threshold| Method | Best For | Assumption |

|---|---|---|

| IQR | Any distribution, robust | None (non-parametric) |

| Z-Score | Normal distribution | Gaussian data |

| Modified Z-Score | Skewed data | Uses median instead of mean |

3. ML-Based Methods (High-Dimensional Data)

| Method | How It Works | When to Use |

|---|---|---|

| Isolation Forest | Isolates outliers with random splits | High-dimensional, mixed features |

| DBSCAN | Points not in any cluster are outliers | Spatial data, unknown # of clusters |

| LOF (Local Outlier Factor) | Compares local density to neighbors | Varying density regions |

| Mahalanobis Distance | Accounts for feature correlations | Multivariate, correlated features |

| Autoencoders | High reconstruction error = outlier | Complex patterns, deep learning |

from sklearn.ensemble import IsolationForest

# Isolation Forest for high-dimensional data

clf = IsolationForest(contamination=0.1, random_state=42)

outlier_labels = clf.fit_predict(X) # -1 for outliers, 1 for inliersHandling Strategies

Once outliers are detected, you have several options:

| Strategy | When to Use | How |

|---|---|---|

| Remove | True errors, data corruption | Delete outlier rows |

| Cap/Winsorize | Keep data, limit influence | Clip to percentiles (e.g., 1st/99th) |

| Transform | Reduce skewness | Apply log, sqrt, Box-Cox |

| Impute | Treat as missing | Replace with median/mode |

| Keep | True rare events | Use robust methods |

# Winsorization: Cap at percentiles

from scipy.stats import mstats

def winsorize(data, limits=(0.01, 0.01)):

"""Cap outliers at 1st and 99th percentiles"""

return mstats.winsorize(data, limits=limits)

# Log transform: Reduce right skew

def log_transform(data):

return np.log1p(data) # log(1+x) handles zerosMaking Models Robust to Outliers

1. Use Robust Loss Functions

| Loss | Robustness | When to Use |

|---|---|---|

| MSE | ❌ Not robust | Clean data, Gaussian errors |

| MAE | ✅ Robust | Some outliers expected |

| Huber | ✅ Hybrid | MSE for small errors, MAE for large |

| Quantile | ✅ Very robust | Regression with heavy-tailed errors |

# Huber loss: MSE for small errors, MAE for large

import torch.nn as nn

criterion = nn.HuberLoss(delta=1.0) # delta controls transition point2. Use Robust Scaling

from sklearn.preprocessing import RobustScaler

# Uses median and IQR instead of mean and std

# Much less affected by outliers than StandardScaler

scaler = RobustScaler() # (x - median) / IQR

X_scaled = scaler.fit_transform(X)3. Choose Robust Algorithms

| Robust | Not Robust |

|---|---|

| Tree-based (Random Forest, XGBoost) | Linear Regression |

| Median-based methods | Mean-based methods |

| Huber Regression | OLS Regression |

| k-Medoids | k-Means |

4. Regularization Helps

Regularization reduces variance and makes models less sensitive to individual points:

- L2 (Ridge): Shrinks weights, reduces influence of any single feature

- Dropout: Random neuron dropping prevents over-reliance on specific patterns

Interview Q: “Why are tree-based models robust to outliers?”

A: Tree-based models (Random Forest, XGBoost) split data based on thresholds, not magnitudes. A value of 100 vs 1,000,000 might fall in the same leaf node if they’re both above the split threshold. The prediction depends on which leaf the point lands in, not the exact value. This makes trees naturally robust to outliers—unlike linear models where outliers directly pull the regression line.

Quick Decision Guide

Outlier detected?

│

├── Is it a data error?

│ │

│ ├── YES → Remove or impute

│ │

│ └── NO (rare but valid)

│ │

│ ├── Use robust methods (MAE, Huber, trees)

│ └── Or winsorize/cap if you must use non-robust methods

│

└── Not sure?

│

└── 1. Investigate the data point

2. Try both with/without

3. Use cross-validation to decide1.10 Loss Function Comparison

The loss function (also called cost function or objective function) is arguably the most important design choice in machine learning—it defines exactly what “good” means for your model. During training, the optimizer’s sole job is to minimize this function, so your model will learn whatever behavior the loss function rewards.

Why does loss function choice matter so much?

Defines the learning signal: The gradients that update your weights come from the loss. Choose the wrong loss, and your model receives misleading gradients that don’t guide it toward the right solution.

Must match your task:

- Regression (predict continuous values): Use MSE, MAE, or Huber

- Classification (predict categories): Use Cross-Entropy (binary or categorical)

- Using MSE for classification can fail spectacularly—see below!

Affects optimization dynamics: Some losses have better gradient properties than others. Cross-entropy gives clean gradients for classification; MSE with sigmoid can cause vanishing gradients.

How to think about it: The loss function is a contract between you and the optimizer. You specify “minimize this number,” and the optimizer will find weights that do exactly that—even if that’s not what you actually wanted. Choosing the right loss ensures that minimizing the number also means solving your actual problem.

Quick Reference Table

| Loss Function | Task | Output Activation | Formula |

|---|---|---|---|

| MSE | Regression | None (linear) | \(\frac{1}{N}\sum(y - \hat{y})^2\) |

| MAE | Regression | None | \(\frac{1}{N}\sum|y - \hat{y}|\) |

| Binary CE | Binary classification | Sigmoid | \(-[y\log\hat{y} + (1-y)\log(1-\hat{y})]\) |

| Categorical CE | Multi-class | Softmax | \(-\sum_k y_k \log \hat{y}_k\) |

| Hinge | Binary (SVM) | None | \(\max(0, 1 - y \cdot \hat{y})\) |

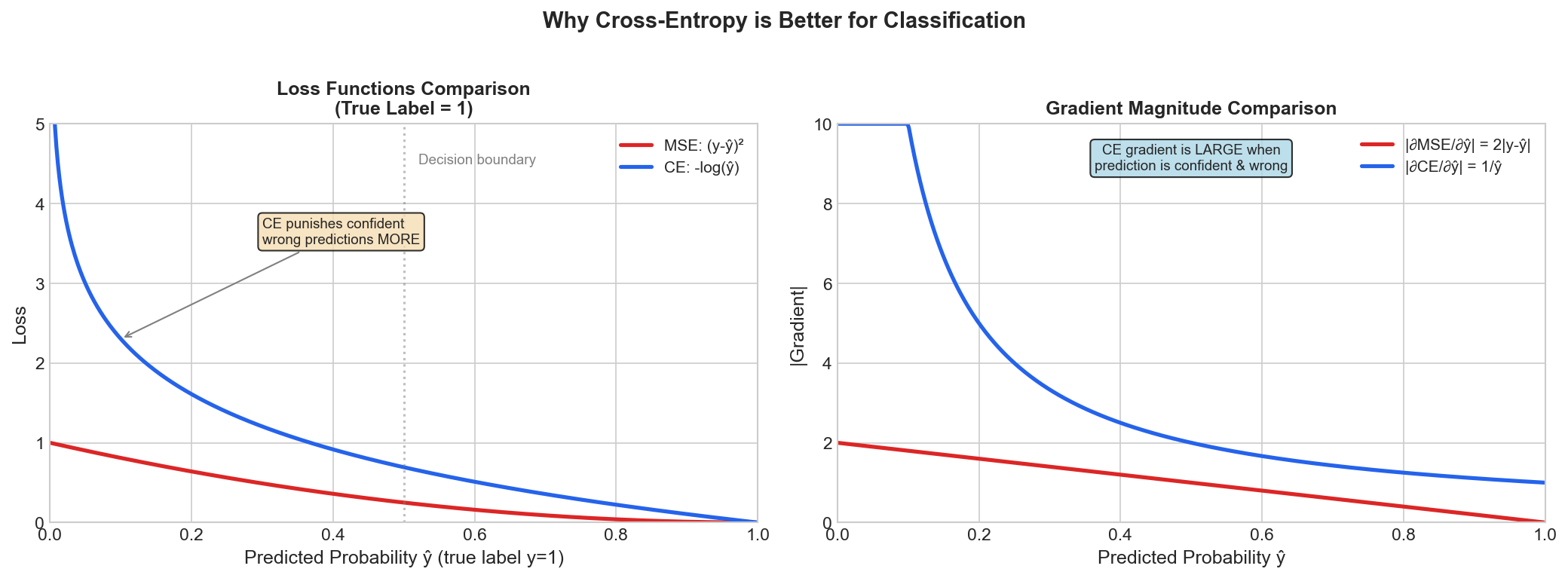

MSE vs Cross-Entropy for Classification

Why not MSE for classification?

Figure: Comparison of

Cross-Entropy and MSE loss for classification. Cross-entropy

penalizes confident wrong predictions much more

severely.

Figure: Comparison of

Cross-Entropy and MSE loss for classification. Cross-entropy

penalizes confident wrong predictions much more

severely.

True label: y = 1

Prediction: ŷ = 0.99 (very confident, correct)

MSE: (1 - 0.99)² = 0.0001

CE: -log(0.99) = 0.01

Prediction: ŷ = 0.01 (very confident, WRONG!)

MSE: (1 - 0.01)² = 0.98

CE: -log(0.01) = 4.6 ← Much stronger penalty!Cross-entropy penalizes confident wrong predictions much more heavily!

MSE Gradient Problem

For sigmoid output with MSE: \[\frac{\partial \text{MSE}}{\partial z} \propto \sigma(z)(1-\sigma(z))\]

When \(\sigma(z) \approx 0\) or \(\sigma(z) \approx 1\): gradient vanishes!

For cross-entropy: \[\frac{\partial \text{CE}}{\partial z} = \hat{y} - y\]

No vanishing gradient! Clean, constant-scale updates.

Huber Loss: Best of Both Worlds

\[L_\delta(y, \hat{y}) = \begin{cases} \frac{1}{2}(y - \hat{y})^2 & |y - \hat{y}| \leq \delta \\ \delta|y - \hat{y}| - \frac{1}{2}\delta^2 & |y - \hat{y}| > \delta \end{cases}\]

- MSE for small errors (smooth)

- MAE for large errors (robust to outliers)

1.11 Convolutional Neural Networks (CNNs)

The Problem with MLPs for Images

A 224×224 RGB image has 224 × 224 × 3 = 150,528 input features.

Fully connected layer with 1000 hidden units:

- 150,528 × 1000 = 150 million parameters in first layer alone!

- Doesn’t exploit spatial structure

- No translation invariance

The Convolution Operation

A filter (kernel) slides across the image:

Input (5×5): Filter (3×3): Output (3×3):

┌───┬───┬───┬───┬───┐ ┌───┬───┬───┐

│ 1 │ 2 │ 3 │ 0 │ 1 │ │ 1 │ 0 │-1 │

├───┼───┼───┼───┼───┤ ├───┼───┼───┤

│ 0 │ 1 │ 2 │ 3 │ 2 │ │ 1 │ 0 │-1 │ Slide filter,

├───┼───┼───┼───┼───┤ * ├───┼───┼───┤ → compute dot product

│ 1 │ 0 │ 1 │ 0 │ 1 │ │ 1 │ 0 │-1 │ at each position

├───┼───┼───┼───┼───┤ └───┴───┴───┘

│ 2 │ 1 │ 0 │ 1 │ 2 │

├───┼───┼───┼───┼───┤

│ 1 │ 0 │ 2 │ 1 │ 0 │

└───┴───┴───┴───┴───┘

Example computation (top-left):

1×1 + 2×0 + 3×(-1) + 0×1 + 1×0 + 2×(-1) + 1×1 + 0×0 + 1×(-1) = 1-3-2+1-1 = -4Why Convolutions Work

- Parameter sharing: Same filter used everywhere → fewer parameters

- Local connectivity: Each output depends on small local region

- Translation equivariance: Cat in corner detected same as cat in center

Key CNN Concepts

Stride: How many pixels to move the filter each step

- Stride 1: Output ≈ input size

- Stride 2: Output ≈ half input size

Padding: Add zeros around input to preserve dimensions

- “Same” padding: Output = Input size

- “Valid” padding: No padding, output smaller

Pooling: Downsample by taking max/average over regions

2×2 Max Pool:

┌───┬───┐ ┌───┐

│ 1 │ 3 │ │ 4 │

├───┼───┤ → └───┘

│ 2 │ 4 │

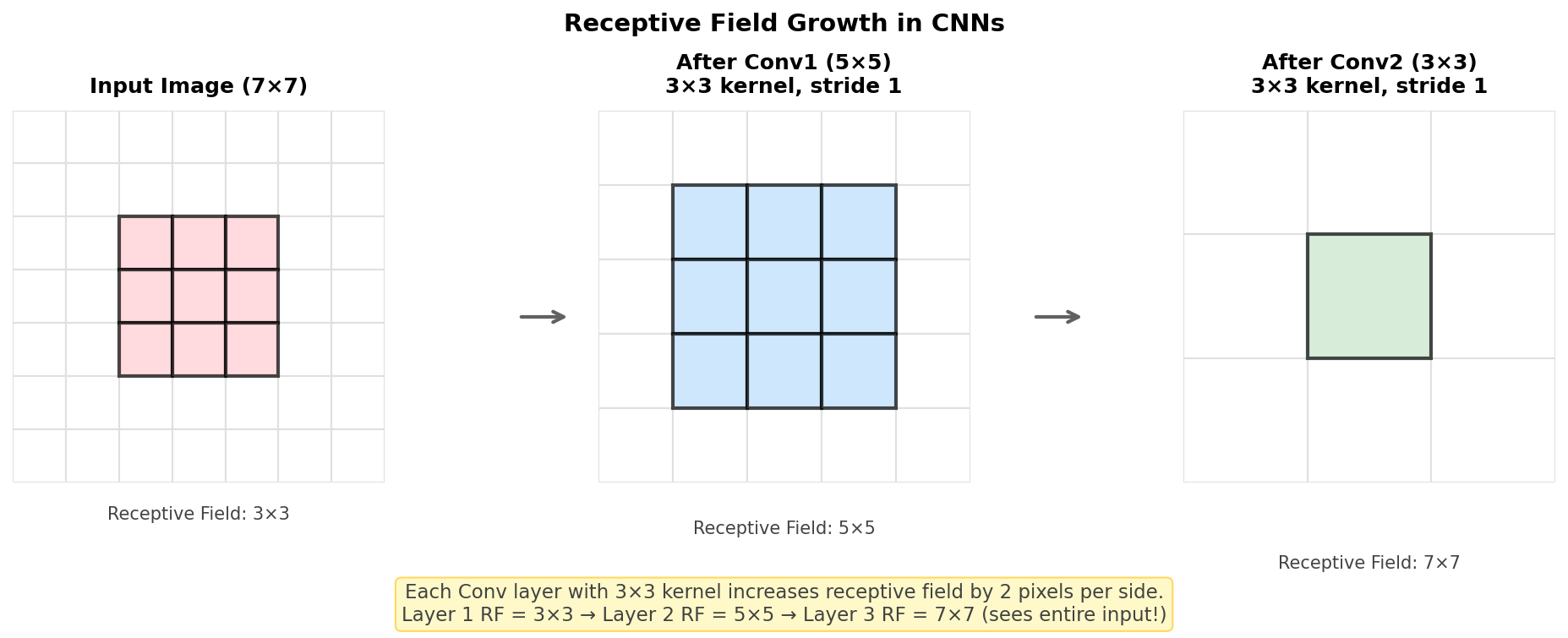

└───┴───┘Receptive Fields: What Each Neuron “Sees”

The receptive field of a neuron is the region of the input image that can influence its output. Understanding receptive fields is crucial for CNN design.

Figure: Receptive field

growth in a CNN. Each 3×3 convolution increases the

receptive field by 2 pixels per side. After 2 layers with

3×3 kernels, a single output neuron “sees” a 5×5 region of

the input.

Figure: Receptive field

growth in a CNN. Each 3×3 convolution increases the

receptive field by 2 pixels per side. After 2 layers with

3×3 kernels, a single output neuron “sees” a 5×5 region of

the input.

Receptive field formula (for stride-1 convolutions):

\[RF_{out} = RF_{in} + (k - 1) \times \prod_{i=1}^{l-1} s_i\]

Where: - \(RF\) = receptive field size - \(k\) = kernel size - \(s_i\) = stride at layer \(i\)

Simplified rule for 3×3 kernels with stride 1: \[RF_l = RF_{l-1} + 2\]

Starting from \(RF_0 = 1\) (single pixel): - After Conv1 (3×3): RF = 3 - After Conv2 (3×3): RF = 5 - After Conv3 (3×3): RF = 7 - After Conv4 (3×3): RF = 9

Why receptive fields matter:

- Feature hierarchy: Early layers have small RFs → detect edges, textures. Deep layers have large RFs → detect objects, scenes

- Network depth: Deeper networks = larger RFs = can capture more global information

- Design tradeoff: Larger kernels (5×5, 7×7) increase RF faster but add more parameters

Interview Q: “Why do modern CNNs use stacked 3×3 convolutions instead of larger kernels?”

A: Two 3×3 convolutions have the same receptive field as one 5×5 (RF = 5), but with: - Fewer parameters: \(2 \times (3^2) = 18\) vs \(5^2 = 25\) - More non-linearity: Two ReLU activations vs one - More representational power

A Simple CNN Architecture

Input: 32×32×3 (e.g., CIFAR-10 image)

↓

Conv: 32 filters, 3×3 → 32×32×32

ReLU

MaxPool 2×2 → 16×16×32

↓

Conv: 64 filters, 3×3 → 16×16×64

ReLU

MaxPool 2×2 → 8×8×64

↓

Flatten → 4096

↓

FC → 256

ReLU

↓

FC → 10 (classes)

SoftmaxPyTorch CNN

import torch.nn as nn

class SimpleCNN(nn.Module):

def __init__(self):

super().__init__()

self.conv1 = nn.Conv2d(3, 32, kernel_size=3, padding=1)

self.conv2 = nn.Conv2d(32, 64, kernel_size=3, padding=1)

self.pool = nn.MaxPool2d(2, 2)

self.fc1 = nn.Linear(64 * 8 * 8, 256)

self.fc2 = nn.Linear(256, 10)

def forward(self, x):

x = self.pool(F.relu(self.conv1(x))) # 32×32 → 16×16

x = self.pool(F.relu(self.conv2(x))) # 16×16 → 8×8

x = x.view(-1, 64 * 8 * 8) # Flatten

x = F.relu(self.fc1(x))

x = self.fc2(x)

return x1.12 Word Embeddings

The Problem: How to Represent Words as Numbers?

Neural networks need numerical inputs. How do we convert words to numbers?

Approach 1: One-Hot Encoding

"cat" → [1, 0, 0, 0]

"dog" → [0, 1, 0, 0]

"bird" → [0, 0, 1, 0]

"fish" → [0, 0, 0, 1]Problems:

- Sparse: V = 50,000 → vectors with 49,999 zeros

- No similarity: cat·dog = 0 (orthogonal), even though semantically related

- Memory: Large vocabulary = huge vectors

Approach 2: Dense Embeddings

Map each word to a dense, low-dimensional vector:

"cat" → [0.2, -0.4, 0.1, 0.8, ...] (d = 300 dimensions)

"dog" → [0.3, -0.3, 0.0, 0.7, ...] (similar to cat!)

"fish" → [-0.5, 0.2, 0.9, -0.1, ...] (different)Why Embeddings Work

Distributional hypothesis: Words that appear in similar contexts have similar meanings.

“The cat sat on the mat” “The dog sat on the mat”

cat and dog appear in similar contexts → similar embeddings!

Embedding Layer in PyTorch

import torch.nn as nn

# Vocabulary of 10,000 words, embedding dimension 300

embedding = nn.Embedding(num_embeddings=10000, embedding_dim=300)

# Convert word indices to embeddings

word_indices = torch.tensor([42, 1337, 99]) # 3 words

word_vectors = embedding(word_indices) # Shape: (3, 300)Pretrained Embeddings

Word2Vec, GloVe: Trained on billions of words

- Capture semantic relationships

- “king” - “man” + “woman” ≈ “queen”

# Using pretrained GloVe

from torchtext.vocab import GloVe

glove = GloVe(name='6B', dim=300)

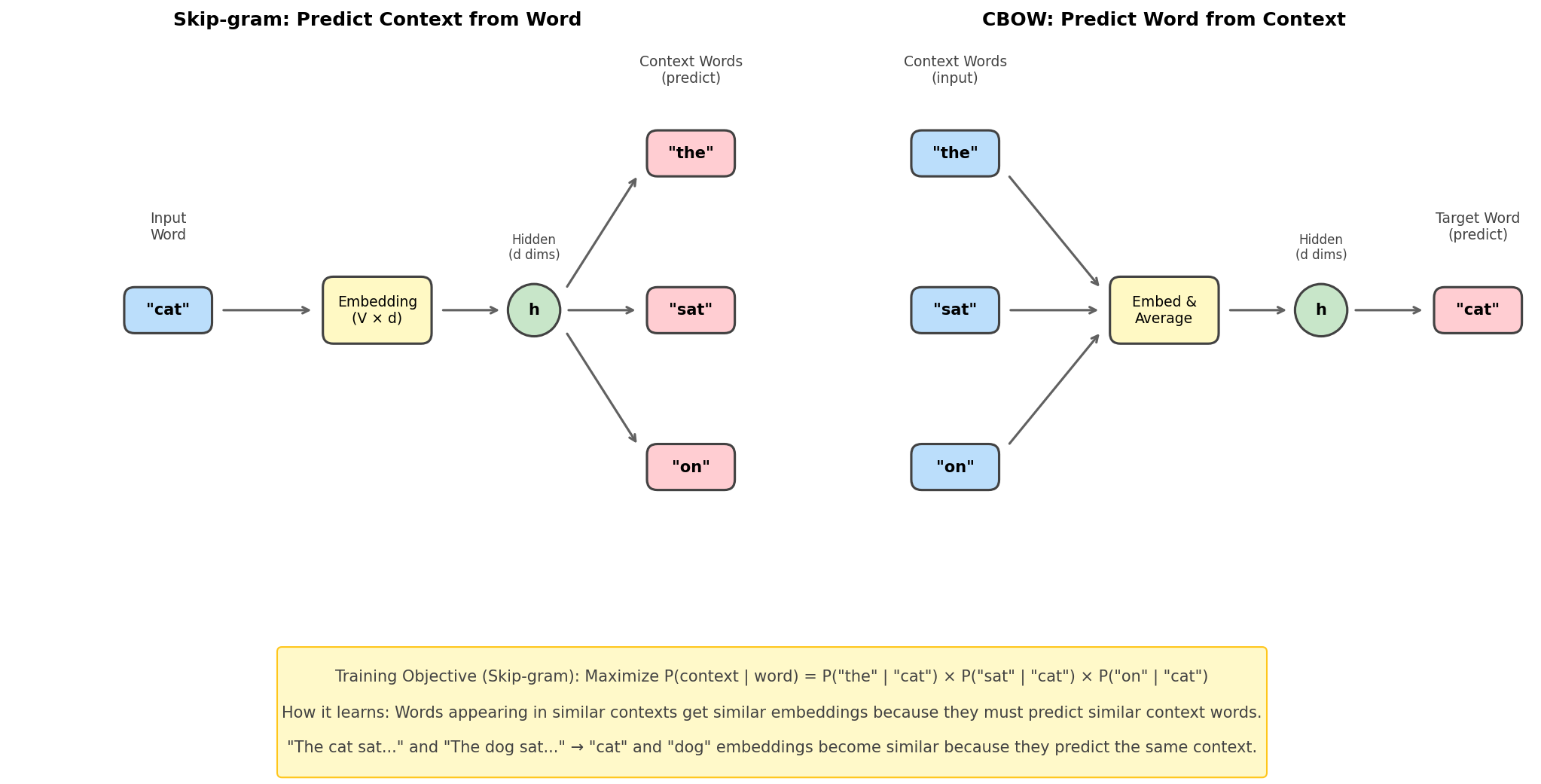

cat_embedding = glove['cat'] # 300-dimensional vectorHow Word2Vec Learns: Skip-gram Training

Understanding how Word2Vec learns embeddings provides deep insight into self-supervised learning—the foundation of modern LLMs.

Figure: Skip-gram and

CBOW architectures. Skip-gram predicts context words from

the center word; CBOW predicts the center word from

context.

Figure: Skip-gram and

CBOW architectures. Skip-gram predicts context words from

the center word; CBOW predicts the center word from

context.

The Skip-gram Objective

Given a center word, predict its surrounding context words:

\[\text{maximize} \quad \sum_{t=1}^{T} \sum_{-c \leq j \leq c, j \neq 0} \log P(w_{t+j} | w_t)\]

Where \(c\) is the context window size.

The probability model:

\[P(w_O | w_I) = \frac{\exp(v'_{w_O} \cdot v_{w_I})}{\sum_{w=1}^{V} \exp(v'_w \cdot v_{w_I})}\]

This is just a softmax! The dot product measures similarity between: - \(v_{w_I}\): Input embedding of the center word - \(v'_{w_O}\): Output embedding of the context word

Why this learns semantic similarity:

The training signal “predict context from word” forces words appearing in similar contexts to have similar embeddings. Consider:

"The cat sat on the mat"

"The dog sat on the mat"Both “cat” and “dog” must predict the same context words (“the”, “sat”, “on”, “mat”), so they’re pushed to have similar embeddings!

Negative Sampling (Practical Training)

The full softmax over vocabulary is expensive (V can be 100,000+). Negative sampling approximates it:

Instead of computing the full softmax, contrast the positive (real) context word against random “negative” words:

\[\mathcal{L} = \log \sigma(v'_{w_O} \cdot v_{w_I}) + \sum_{i=1}^{k} \mathbb{E}_{w_i \sim P_n(w)} [\log \sigma(-v'_{w_i} \cdot v_{w_I})]\]

- First term: Push the real context word embedding closer to center word

- Second term: Push random noise words away from center word

- Typically \(k = 5\)-20 negative samples

This is contrastive learning! The same principle underlies modern self-supervised methods like SimCLR and CLIP.

From Word Embeddings to Transformers

Modern LLMs don’t use fixed word embeddings:

- Subword tokenization: “unhappiness” → [“un”, “happiness”]

- Contextual embeddings: Same word, different meaning in context

- Learned during pretraining: Not pretrained separately

Static embedding (Word2Vec):

"bank" → same vector always

Contextual embedding (BERT, GPT):

"river bank" → one vector

"bank account" → different vector!1.13 The XOR Problem: A Complete MLP Example

Why XOR?

XOR is the classic example showing why we need hidden layers:

| \(x_1\) | \(x_2\) | \(y\) (XOR) |

|---|---|---|

| 0 | 0 | 0 |

| 0 | 1 | 1 |

| 1 | 0 | 1 |

| 1 | 1 | 0 |

No single line can separate the classes! (It’s not linearly separable)

x₂

↑

1 │ ● ○ ← Can't draw one line

│ to separate ● from ○

0 │ ○ ●

└──────────────→ x₁

0 1The Network Architecture

Input Layer Hidden Layer (2 neurons) Output Layer

x₁ ─────┐

├───→ h₁ ─────┐

x₂ ─────┤ ├───→ y

├───→ h₂ ─────┘

1 (bias)─┘Dimensions:

- Input: 2 features

- Hidden: 2 neurons (with ReLU)

- Output: 1 neuron (with sigmoid)

Step 1: Initialize Weights

Let’s use specific weights that solve XOR:

Hidden layer weights \(W^{(1)}\) and biases \(b^{(1)}\): \[W^{(1)} = \begin{bmatrix} 1 & 1 \\ 1 & 1 \end{bmatrix}, \quad b^{(1)} = \begin{bmatrix} 0 \\ -1 \end{bmatrix}\]

Output layer weights \(W^{(2)}\) and bias \(b^{(2)}\): \[W^{(2)} = \begin{bmatrix} 1 \\ -2 \end{bmatrix}, \quad b^{(2)} = 0\]

Step 2: Forward Pass (for input [1, 1])

Hidden layer pre-activation: \[z^{(1)} = W^{(1)} \begin{bmatrix} 1 \\ 1 \end{bmatrix} + b^{(1)} = \begin{bmatrix} 1 \cdot 1 + 1 \cdot 1 \\ 1 \cdot 1 + 1 \cdot 1 \end{bmatrix} + \begin{bmatrix} 0 \\ -1 \end{bmatrix} = \begin{bmatrix} 2 \\ 1 \end{bmatrix}\]

Hidden layer activation (ReLU): \[h = \text{ReLU}(z^{(1)}) = \begin{bmatrix} \max(0, 2) \\ \max(0, 1) \end{bmatrix} = \begin{bmatrix} 2 \\ 1 \end{bmatrix}\]

Output layer pre-activation: \[z^{(2)} = W^{(2)T} h + b^{(2)} = 1 \cdot 2 + (-2) \cdot 1 + 0 = 0\]

Output (sigmoid): \[\hat{y} = \sigma(0) = \frac{1}{1 + e^0} = 0.5\]

Step 3: All Four Inputs

| Input \((x_1, x_2)\) | \(z^{(1)}\) | \(h\) (ReLU) | \(z^{(2)}\) | \(\hat{y}\) | Target \(y\) |

|---|---|---|---|---|---|

| (0, 0) | (0, -1) | (0, 0) | 0 | 0.5 | 0 |

| (0, 1) | (1, 0) | (1, 0) | 1 | 0.73 | 1 |

| (1, 0) | (1, 0) | (1, 0) | 1 | 0.73 | 1 |

| (1, 1) | (2, 1) | (2, 1) | 0 | 0.5 | 0 |

Better-Tuned Weights for XOR

The weights above give outputs at 0.5 for (0,0) and (1,1) — not ideal. Here are better weights that give outputs closer to 0 and 1:

Optimal hidden layer weights \(W^{(1)}\) and biases \(b^{(1)}\): \[W^{(1)} = \begin{bmatrix} 20 & 20 \\ 20 & 20 \end{bmatrix}, \quad b^{(1)} = \begin{bmatrix} -10 \\ -30 \end{bmatrix}\]

Optimal output layer weights \(W^{(2)}\) and bias \(b^{(2)}\): \[W^{(2)} = \begin{bmatrix} 20 \\ -20 \end{bmatrix}, \quad b^{(2)} = -10\]

With these weights:

| Input \((x_1, x_2)\) | \(z^{(1)}\) | \(h\) (ReLU) | \(z^{(2)}\) | \(\hat{y}\) | Target \(y\) |

|---|---|---|---|---|---|

| (0, 0) | (-10, -30) | (0, 0) | -10 | 0.00005 ≈ 0 | 0 ✓ |

| (0, 1) | (10, -10) | (10, 0) | 190 | 1.0 ≈ 1 | 1 ✓ |

| (1, 0) | (10, -10) | (10, 0) | 190 | 1.0 ≈ 1 | 1 ✓ |

| (1, 1) | (30, 10) | (30, 10) | 390 | 0.00005 ≈ 0 | 0 ✓ |

Intuition behind these weights: - Hidden neuron 1: \(h_1 = \text{ReLU}(20x_1 + 20x_2 - 10)\) fires when at least one input is 1 - Hidden neuron 2: \(h_2 = \text{ReLU}(20x_1 + 20x_2 - 30)\) fires only when both inputs are 1 - Output: \(20h_1 - 20h_2 - 10\) is large positive only when \(h_1 > 0\) and \(h_2 = 0\)

Step 4: Compute Loss (Binary Cross-Entropy)

For input (1, 1) with \(\hat{y} = 0.5\), target \(y = 0\):

\[\mathcal{L} = -[y \log(\hat{y}) + (1-y) \log(1-\hat{y})]\]

\[= -[0 \cdot \log(0.5) + 1 \cdot \log(0.5)]\]

\[= -\log(0.5) = 0.693\]

Step 5: Backward Pass

Output layer gradient: \[\frac{\partial \mathcal{L}}{\partial z^{(2)}} = \hat{y} - y = 0.5 - 0 = 0.5\]

Gradient w.r.t. output weights: \[\frac{\partial \mathcal{L}}{\partial W^{(2)}} = h \cdot \frac{\partial \mathcal{L}}{\partial z^{(2)}} = \begin{bmatrix} 2 \\ 1 \end{bmatrix} \cdot 0.5 = \begin{bmatrix} 1.0 \\ 0.5 \end{bmatrix}\]

Gradient flowing to hidden layer: \[\frac{\partial \mathcal{L}}{\partial h} = W^{(2)} \cdot \frac{\partial \mathcal{L}}{\partial z^{(2)}} = \begin{bmatrix} 1 \\ -2 \end{bmatrix} \cdot 0.5 = \begin{bmatrix} 0.5 \\ -1.0 \end{bmatrix}\]

Through ReLU (gradient is 1 where input > 0, else 0): \[\frac{\partial \mathcal{L}}{\partial z^{(1)}} = \frac{\partial \mathcal{L}}{\partial h} \odot \mathbf{1}_{z^{(1)} > 0} = \begin{bmatrix} 0.5 \\ -1.0 \end{bmatrix} \odot \begin{bmatrix} 1 \\ 1 \end{bmatrix} = \begin{bmatrix} 0.5 \\ -1.0 \end{bmatrix}\]

Gradient w.r.t. hidden weights: \[\frac{\partial \mathcal{L}}{\partial W^{(1)}} = \frac{\partial \mathcal{L}}{\partial z^{(1)}} \cdot x^T = \begin{bmatrix} 0.5 \\ -1.0 \end{bmatrix} \cdot \begin{bmatrix} 1 & 1 \end{bmatrix} = \begin{bmatrix} 0.5 & 0.5 \\ -1.0 & -1.0 \end{bmatrix}\]

PyTorch Implementation

import torch

import torch.nn as nn

# XOR data

X = torch.tensor([[0, 0], [0, 1], [1, 0], [1, 1]], dtype=torch.float32)

y = torch.tensor([[0], [1], [1], [0]], dtype=torch.float32)

# Network

model = nn.Sequential(

nn.Linear(2, 2),

nn.ReLU(),

nn.Linear(2, 1),

nn.Sigmoid()

)

criterion = nn.BCELoss()

optimizer = torch.optim.SGD(model.parameters(), lr=1.0)

# Training

for epoch in range(1000):

y_pred = model(X)

loss = criterion(y_pred, y)

optimizer.zero_grad()

loss.backward()

optimizer.step()

if epoch % 200 == 0:

print(f"Epoch {epoch}, Loss: {loss.item():.4f}")

# Test

print("\nPredictions:")

print(model(X).detach().round()) # Should be [[0], [1], [1], [0]]Key Insights

- Hidden layer creates new representation: The hidden layer transforms the space so that XOR becomes linearly separable

- Non-linearity is essential: Without ReLU, two linear layers collapse to one

- Backprop chain rule: Gradients flow backward through each layer

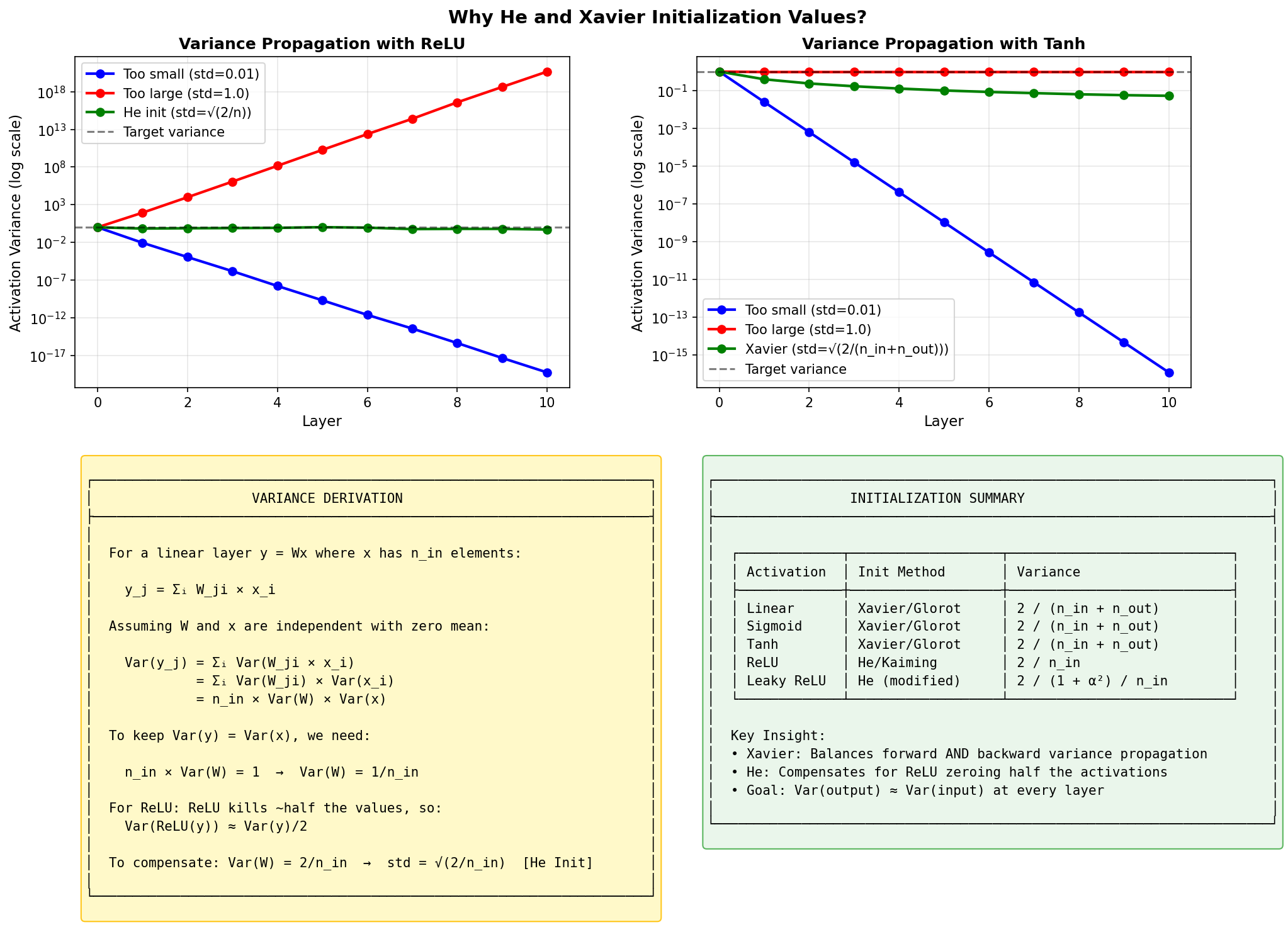

1.14 Weight Initialization

Why Does Initialization Matter?

Bad initialization leads to:

- All zeros: All neurons compute the same thing, learn the same features (symmetry problem)

- Too small: Activations shrink to zero layer by layer (vanishing signals)

- Too large: Activations explode, gradients explode

The Goal

Keep activations and gradients at reasonable scale throughout the network.

Xavier/Glorot Initialization (2010)

For tanh/sigmoid activations:

\[W \sim \mathcal{N}\left(0, \frac{2}{n_{\text{in}} + n_{\text{out}}}\right) \quad \text{or} \quad W \sim \mathcal{U}\left(-\sqrt{\frac{6}{n_{\text{in}} + n_{\text{out}}}}, \sqrt{\frac{6}{n_{\text{in}} + n_{\text{out}}}}\right)\]

Intuition: Balance the variance of inputs and outputs so signal doesn’t explode or vanish.

# PyTorch

nn.init.xavier_uniform_(layer.weight)

nn.init.xavier_normal_(layer.weight)He/Kaiming Initialization (2015)

For ReLU activations (ReLU kills half the signal, so we compensate):

\[W \sim \mathcal{N}\left(0, \frac{2}{n_{\text{in}}}\right)\]

Why factor of 2? ReLU zeroes out negative half, so variance is halved. We double the initial variance to compensate.

Deriving He Initialization: Variance Propagation

Let’s derive why He initialization uses \(\text{Var}(W) = \frac{2}{n_{in}}\) for ReLU networks.

Figure: How activation

variance propagates through layers. Without proper

initialization, variance either explodes or vanishes

exponentially. The goal: keep Var(y) ≈ Var(x) at each

layer.

Figure: How activation

variance propagates through layers. Without proper

initialization, variance either explodes or vanishes

exponentially. The goal: keep Var(y) ≈ Var(x) at each

layer.

Setup: Consider a single layer \(y = Wx + b\) where: - Input \(x\) has \(n_{in}\) components, each with variance \(\text{Var}(x_j)\) - Weights \(W_{ij} \sim \mathcal{N}(0, \sigma_w^2)\) are independent of inputs - We want \(\text{Var}(y_i) = \text{Var}(x_j)\) (preserve variance)

Step 1: Variance of one output neuron (before activation)

\[y_i = \sum_{j=1}^{n_{in}} W_{ij} x_j + b_i\]

For zero-mean \(x\) and \(W\), assuming independence:

\[\text{Var}(y_i) = \sum_{j=1}^{n_{in}} \text{Var}(W_{ij} x_j) = \sum_{j=1}^{n_{in}} \text{Var}(W_{ij}) \cdot \text{Var}(x_j) = n_{in} \cdot \sigma_w^2 \cdot \text{Var}(x)\]

Step 2: Preserve variance (Xavier derivation)

For \(\text{Var}(y) = \text{Var}(x)\), we need: \[n_{in} \cdot \sigma_w^2 = 1 \implies \sigma_w^2 = \frac{1}{n_{in}}\]

This is Xavier initialization — perfect for linear layers or tanh (which is approximately linear near 0).

Step 3: Account for ReLU (He derivation)

ReLU zeros out negative values. For zero-mean Gaussian input, exactly half the values are negative:

\[\text{ReLU}(y) = \begin{cases} y & \text{if } y > 0 \\ 0 & \text{if } y \leq 0 \end{cases}\]

The variance after ReLU is halved: \[\text{Var}(\text{ReLU}(y)) = \frac{1}{2} \text{Var}(y)\]

To compensate, we need twice the initial variance:

\[\sigma_w^2 = \frac{2}{n_{in}}\]

This is He/Kaiming initialization!

Why this matters: Without this factor of 2, variance shrinks by half at each layer. After 10 layers: \(0.5^{10} \approx 0.001\) — activations become tiny, gradients vanish.

# PyTorch (default for nn.Linear with ReLU)

nn.init.kaiming_uniform_(layer.weight, nonlinearity='relu')

nn.init.kaiming_normal_(layer.weight, nonlinearity='relu')Quick Reference

| Activation | Initialization | Variance |

|---|---|---|

| Sigmoid/Tanh | Xavier | \(\frac{2}{n_{in} + n_{out}}\) |

| ReLU | He/Kaiming | \(\frac{2}{n_{in}}\) |

| Linear (no activation) | Xavier | \(\frac{2}{n_{in} + n_{out}}\) |

What About Biases?

Almost always initialize to zero:

nn.init.zeros_(layer.bias)Exception: LSTM forget gate biases often initialized to 1 to encourage remembering.

Example: Why Bad Init Fails

# BAD: All zeros

for layer in model.modules():

if hasattr(layer, 'weight'):

layer.weight.data.fill_(0)

# Result: All neurons output the same thing, all gradients identical

# BAD: Too large

for layer in model.modules():

if hasattr(layer, 'weight'):

layer.weight.data.normal_(0, 10)

# Result: Activations explode, NaN losses

# GOOD: He initialization for ReLU network

for layer in model.modules():

if isinstance(layer, nn.Linear):

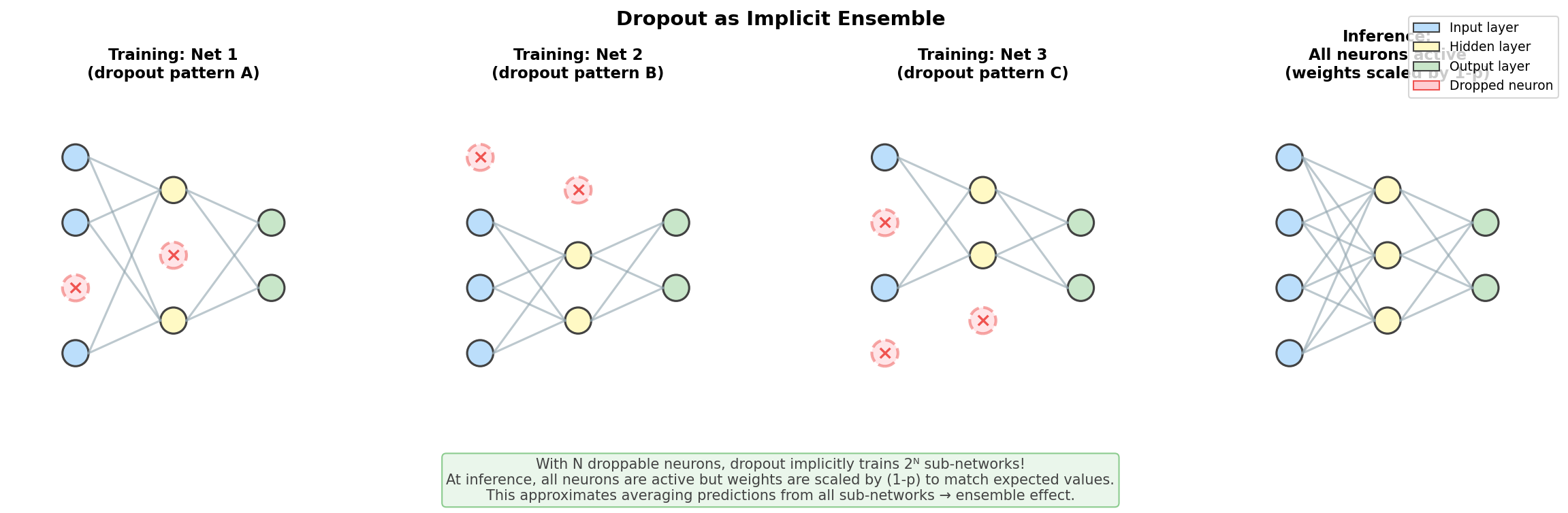

nn.init.kaiming_normal_(layer.weight, nonlinearity='relu')1.15 Dropout

What is Dropout?

During training, randomly set neurons to zero with probability \(p\):

Without dropout: With dropout (p=0.5):